Top Investors and CEOs Appearances: Weekly Roundup

Animal Spirits Ep. 470, Chamath Palihapitiya on The Axios Show, Jeremy Grantham on The Diary Of A CEO, NVIDIA's CEO Jensen Huang & Coherent's CEO Jim Anderson groundbreaking event

Editor’s note: We’re trying a new recurring newsletter that summarizes the key takeaways from appearances by the people shaping markets — across podcasts, interviews, events, and more.

Roundup

A roundup of where top investors and CEOs appeared this week — interviews, podcasts, events, and the topics they discussed.

Podcast and interviews

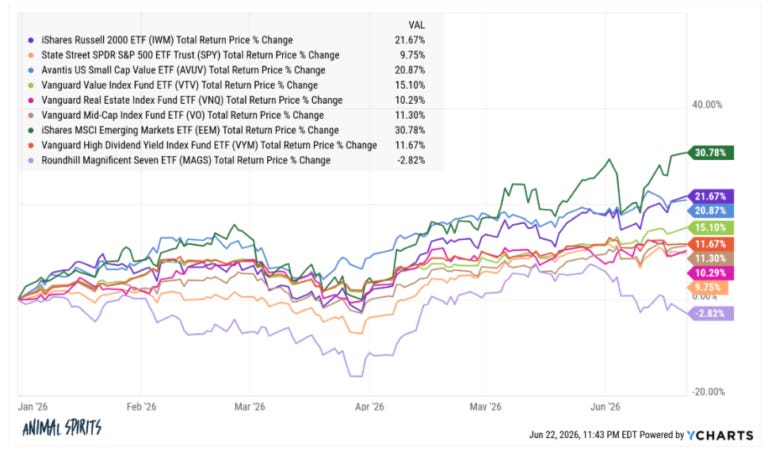

Michael Batnick and Ben Carlson covered market breadth and the Mag7 stumble on Animal Spirits Ep. 470, noting nearly every market segment is outpacing the S&P 500 in 2026. Watch on YouTube.

Chamath Palihapitiya sat down with Dan Primack on The Axios Show (June 25), calling AI “the most important economic leveler of our lifetime” while admitting Meta “fumbled” its AI shot and reflecting on his SPAC era regrets. Watch on YouTube.

Jeremy Grantham, GMO co-founder, told Steven Bartlett on The Diary Of A CEO (June 25) that AI has produced the biggest stock market bubble of his 60-year career, and that he’s sold out of US equities entirely. Watch on YouTube.

Events

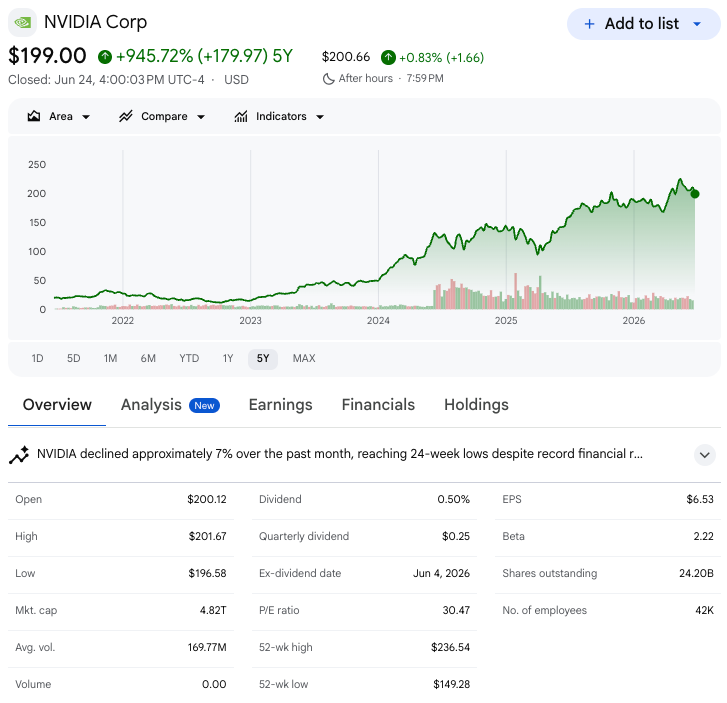

Jensen Huang, Nvidia CEO, joined Coherent CEO Jim Anderson at a groundbreaking ceremony in Sherman, Texas for an expanded indium phosphide laser fab, backed by a $50M CHIPS Act grant, framing it as part of a broader U.S. AI-driven reindustrialization. Watch on YouTube

Deep Dives

Detailed breakdowns of the week’s must-listen investing and finance podcasts — key arguments, notable quotes, and takeaways from each episode, condensed so you can catch up without listening.

Animal Spirits ep. 470: “Everything Is Outperforming the S&P 500 This Year”

June 24, 2026

On episode 470 of Animal Spirits, Michael Batnick and Ben Carlson discuss: why diversification is working again, how AI is creating more winners and losers in the stock market, why the Mag 7 is underperforming, the triple-digit club, why investors are holding more cash, rich people who complain too much, what makes America great, AI is disrupting self help books, the World Cup and more.

Market Breadth: Everyone Beating the S&P

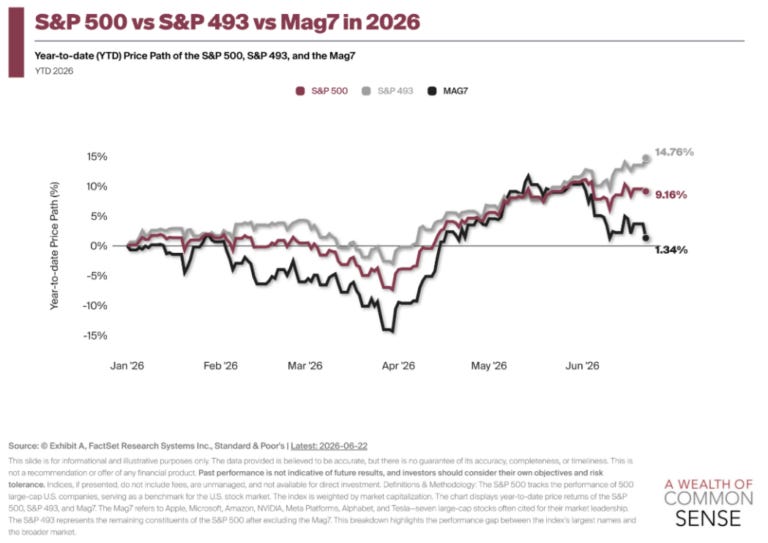

The core theme: nearly every major slice of the market — Russell 2000, small/large cap value, REITs, midcaps, emerging markets, dividend stocks — is outperforming the S&P 500 in 2026, some by wide margins. This is unusual because it’s happening while the S&P itself is up nearly 10% on the year, not while it’s falling (the more typical setup for “diversification working”). The driver is that the Magnificent 7 have stalled out and are no longer pulling the index higher.

Mag7 Drawdowns

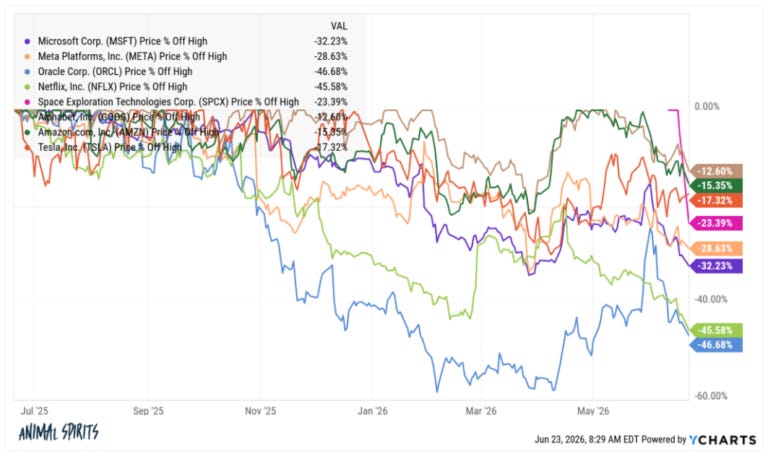

Several mega-cap tech names are deep in drawdown territory even as the broader market does fine: Microsoft down 33%, Meta down almost 30%, Oracle down nearly 50% from highs, Netflix crashing again (Michael holds it, down 30%, says he’d buy more if it falls further), Google down 13%, Amazon down 15%, Tesla down 17%, SpaceX down 25% from its brief post-IPO high. Microsoft, Amazon, and Google are trading at their lowest average P/E in five years. The hosts frame this positively for the overall market: these stocks are shedding the “asset-light, gushing free cash flow” halo as AI capex spending turns them more asset-heavy, and the broadening rally (the “493” outperforming the Mag7) is healthy even if painful for holders of those specific names.

AI Infrastructure / Semiconductor Mania

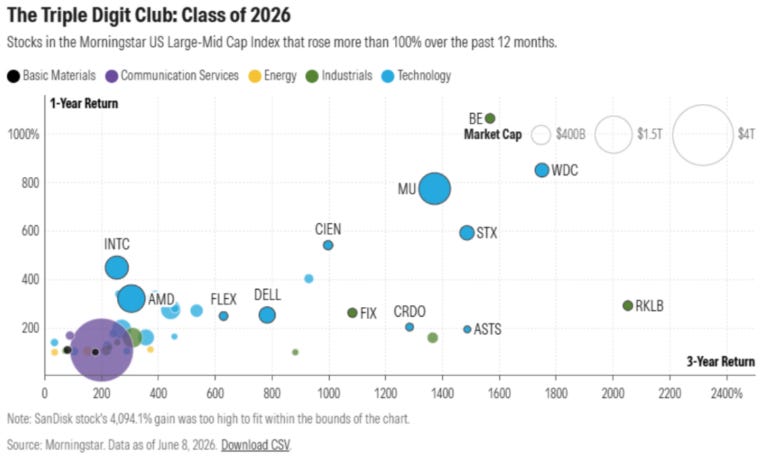

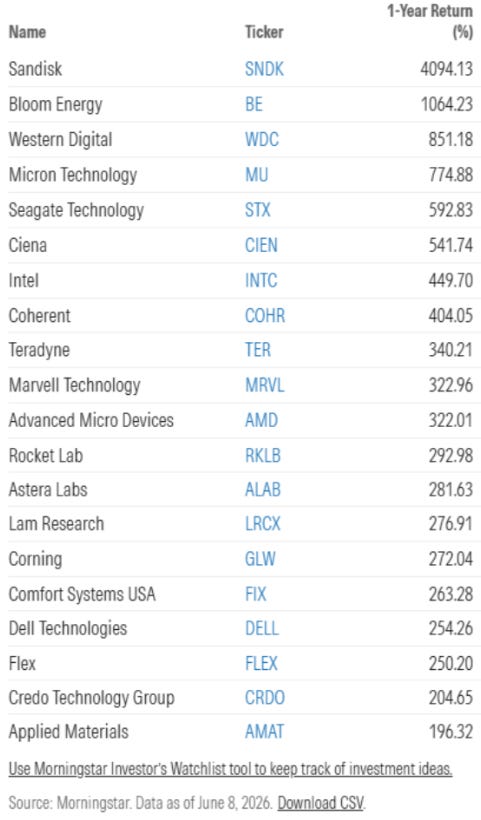

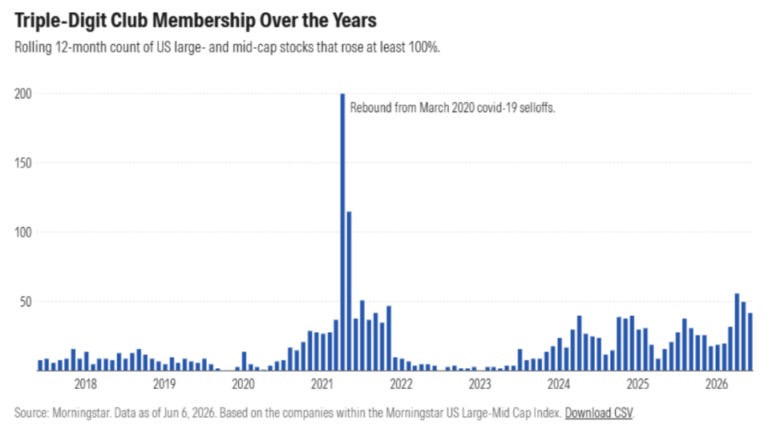

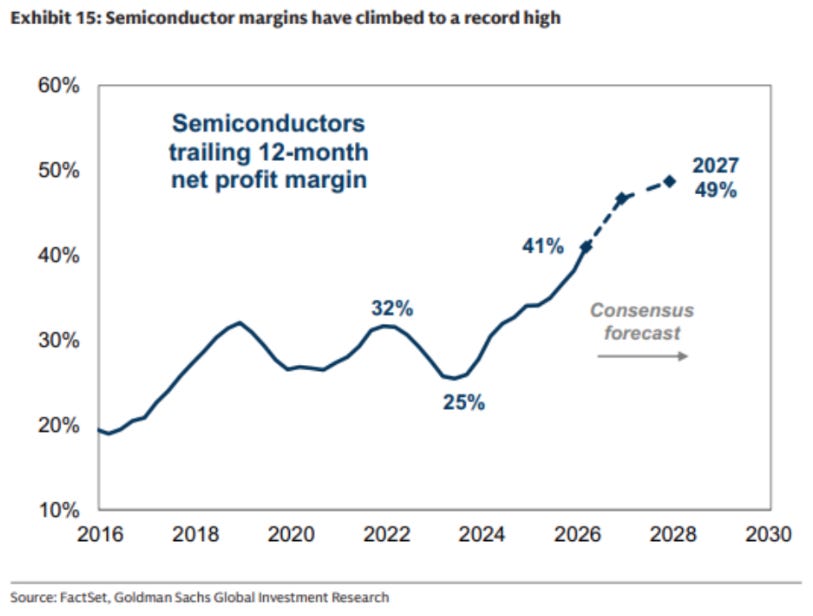

Morningstar found 42 stocks in its large/mid index have more than doubled over the past 12 months (more than 2x the 10-year average), with names like SanDisk, Micron, Western Digital, Dell, and Intel leading — mostly AI infrastructure plays. SK Hynix is up over 300% year-to-date before a recent pullback. Semiconductor net profit margins are projected to rise from a 2024 low of ~25% to 49% by 2027, which the hosts flag as the real story behind the “bubble” framing — fab capacity (e.g., TSMC) can’t scale quickly, creating persistent bottlenecks despite a perceived era of tech abundance.

A Surprising Hedge Lesson

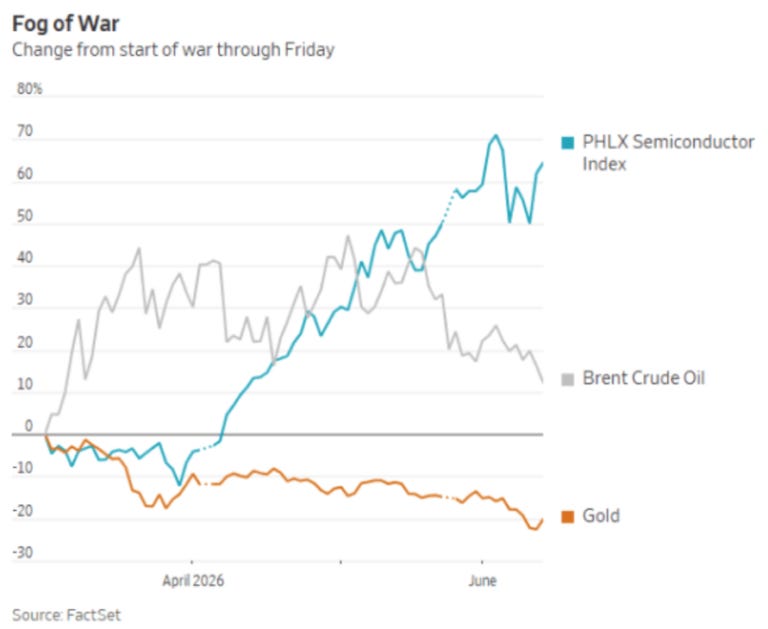

A Wall Street Journal chart tracking gold, oil, and semiconductors since the start of the Middle East war showed semiconductors up 70%, oil only up ~10% (round-tripped most of its spike), and gold down 20% — the opposite of what conventional wisdom would predict for a war hedge. Takeaway: there’s no universal hedge for every scenario.

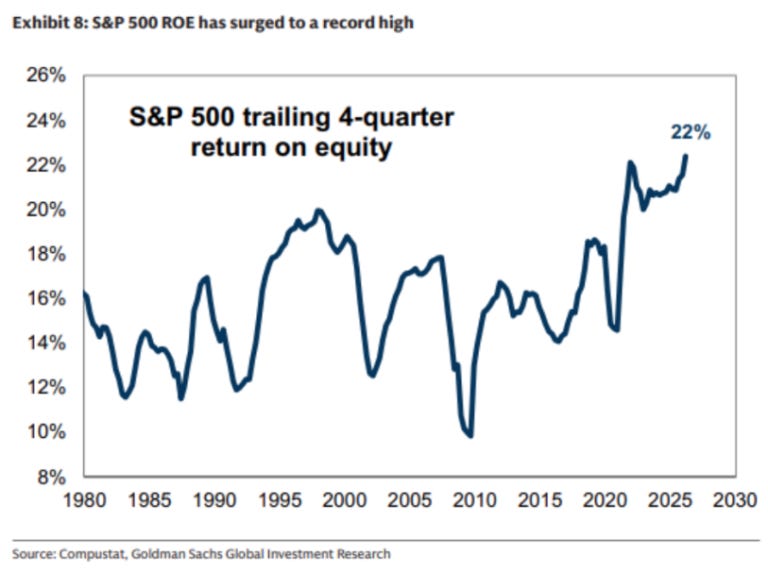

Valuations and Return on Equity

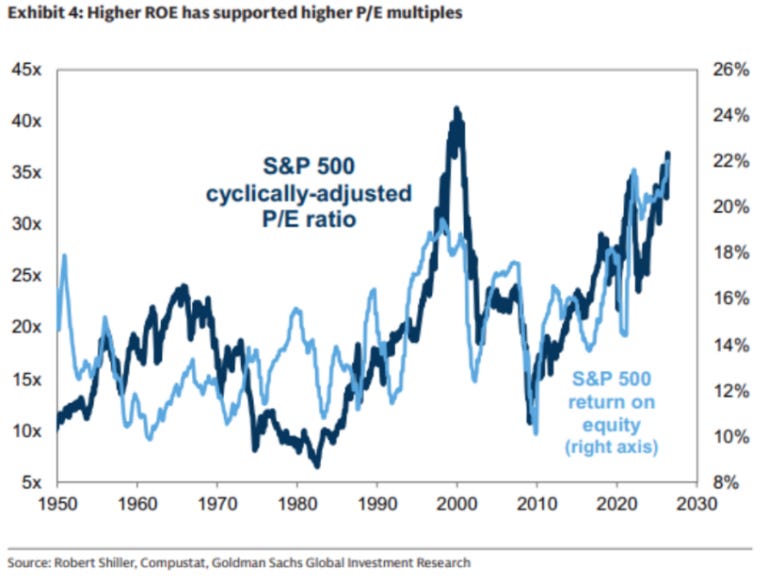

Citing Goldman Sachs research (via Meb Faber’s Idea Farm), the hosts revisit their long-standing argument that higher valuations (CAPE) are justified by structurally higher ROE. Trailing four-quarter ROE has risen to a new historical level this decade, breaking a 45-year cyclical pattern — driven by tech business models. Ben notes Buffett wrote in the 1970s that ROE stays roughly 12-14% over time, which no longer holds. They flag this dynamic may now be reversing for hyperscalers as their margins come under pressure from capex spending.

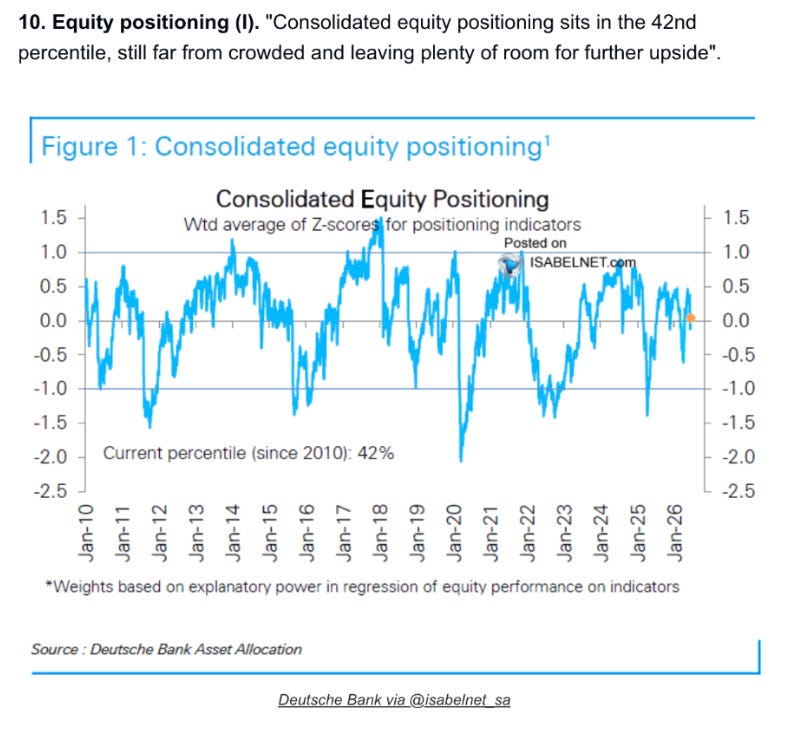

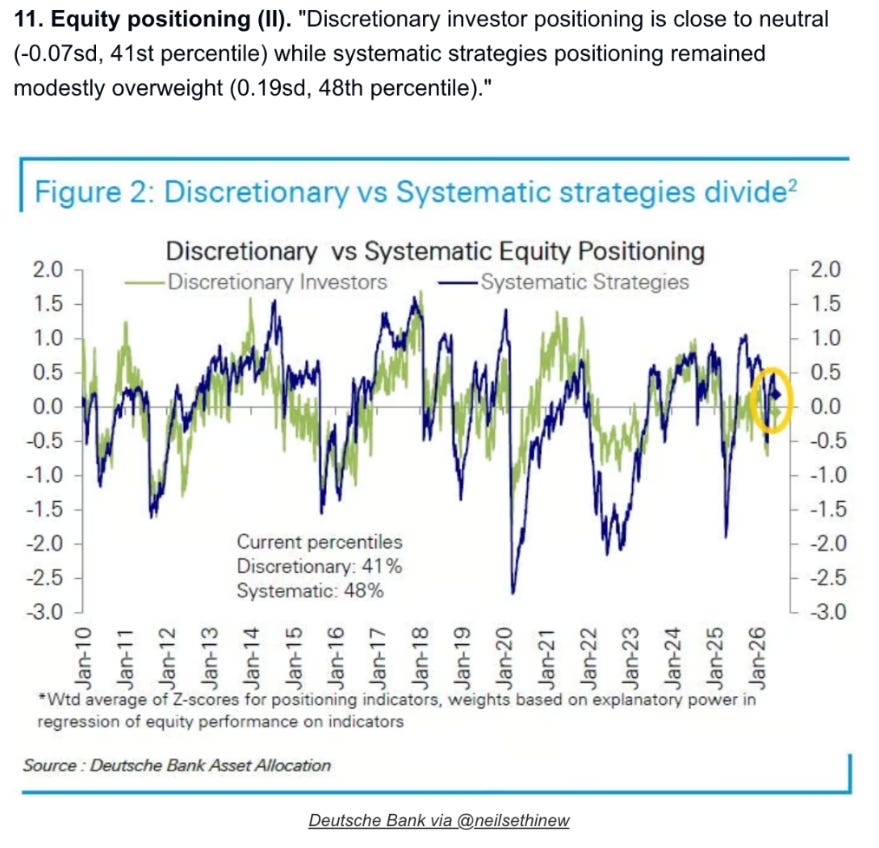

Investor Positioning: Contradictory Signals

A grab-bag of conflicting data points, illustrating the hosts’ broader point that positioning data is noisy and easily cherry-picked to support any narrative:

Citadel Securities: SpaceX’s IPO day was the largest single-day net retail buying event ever recorded by the firm (handles ~35% of US retail volume); 9 of the 10 largest trading days ever happened in the last month.

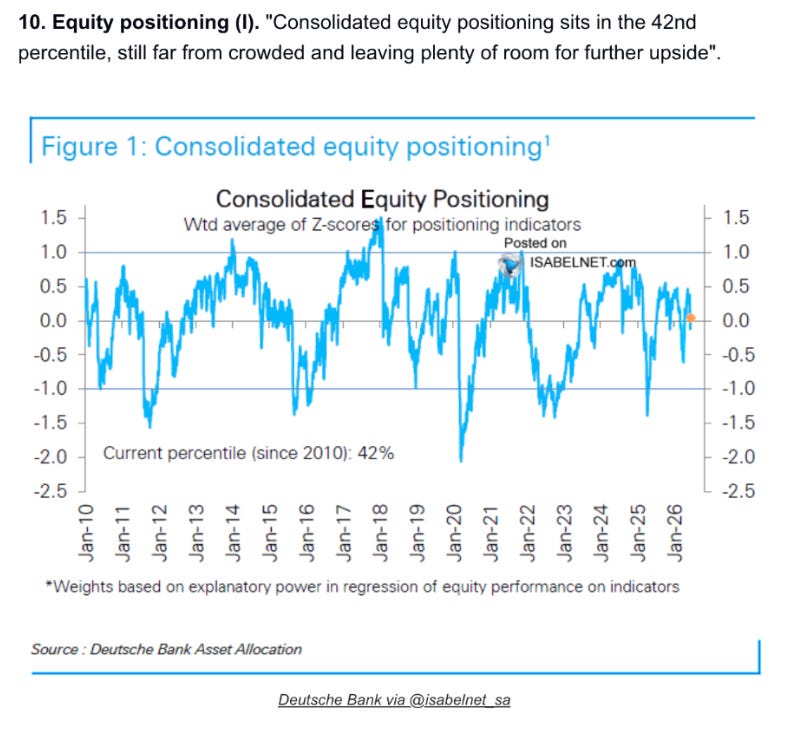

Deutsche Bank consolidated equity positioning sits at just the 42nd percentile — “far from crowded.”

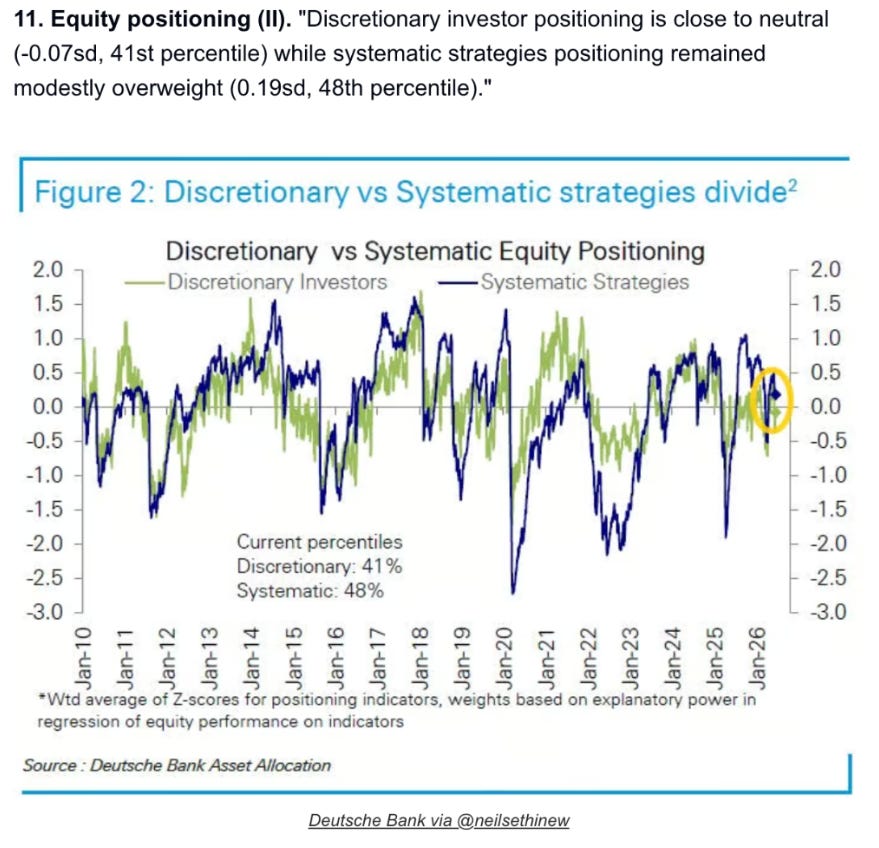

Discretionary investor positioning: 41st percentile; systematic: 40th percentile.

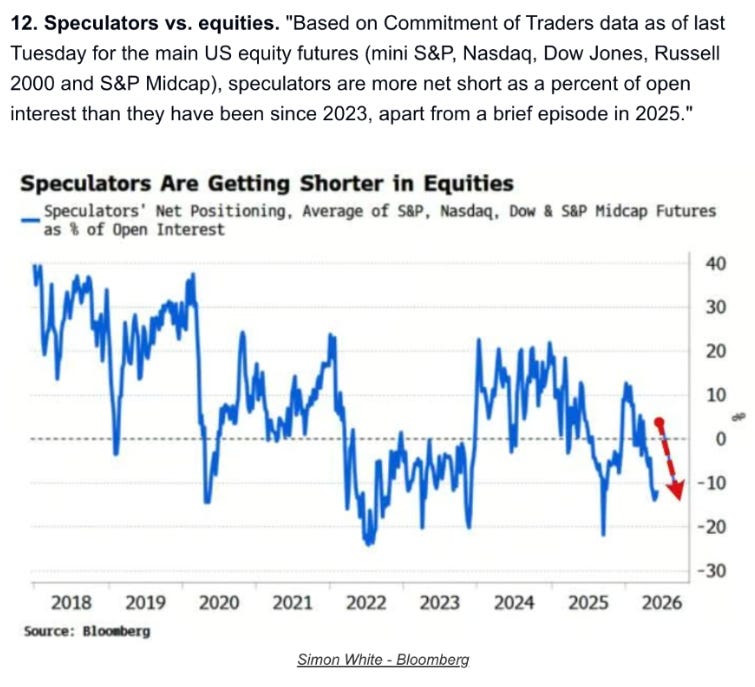

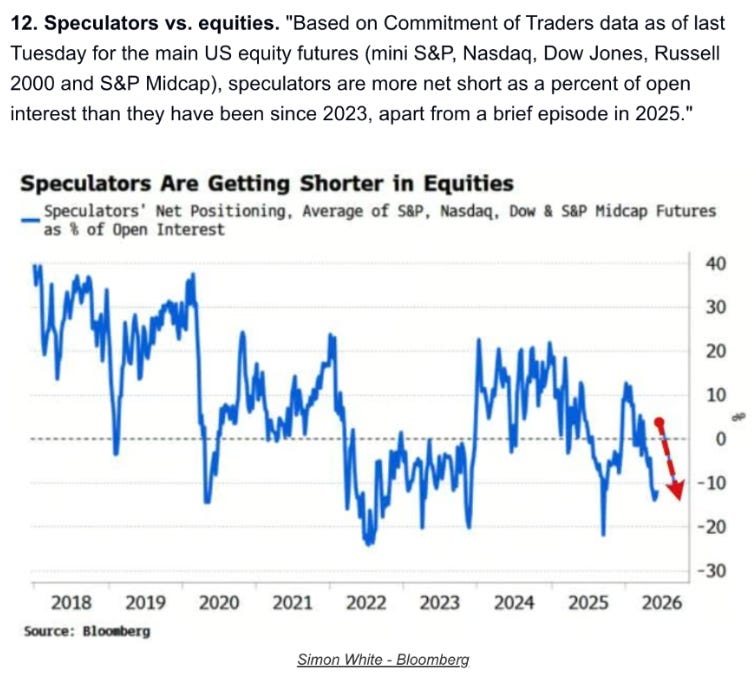

Bloomberg data shows speculators getting shorter in S&P, Nasdaq, Dow, and midcap futures.

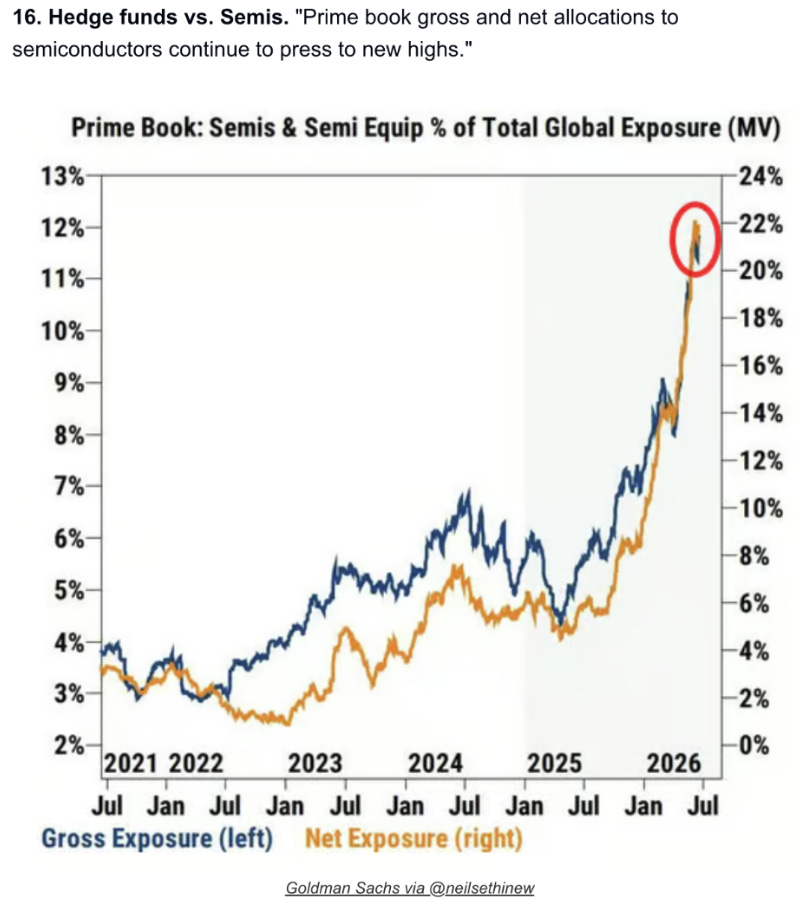

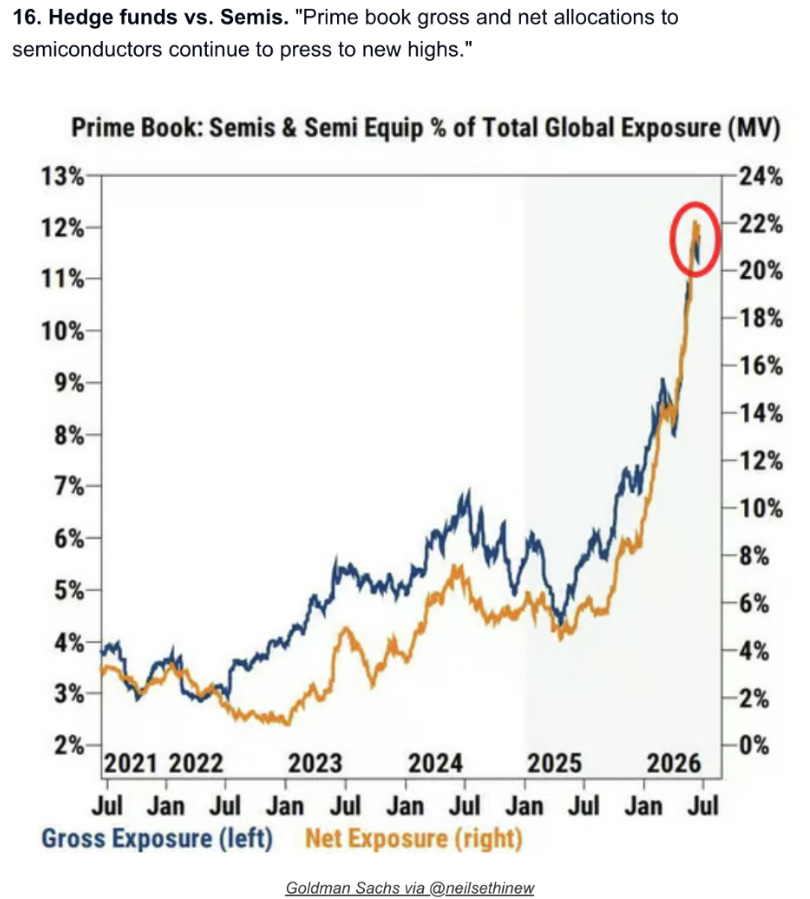

Hedge fund gross/net exposure to semiconductors has gone parabolic — from 8% at the start of the year to 22% now.

Retail flows into semiconductor ETFs are surging (the DRAM ETF doubled from $10B to $20B in a week).

Conversely, Vanda Research data (via Kevin Gordon) shows retail single-stock net buying falling to its lowest level since COVID.

Ben’s takeaway: “Consider the source, not the data — what narrative are they trying to spin?”

Household Cash Levels

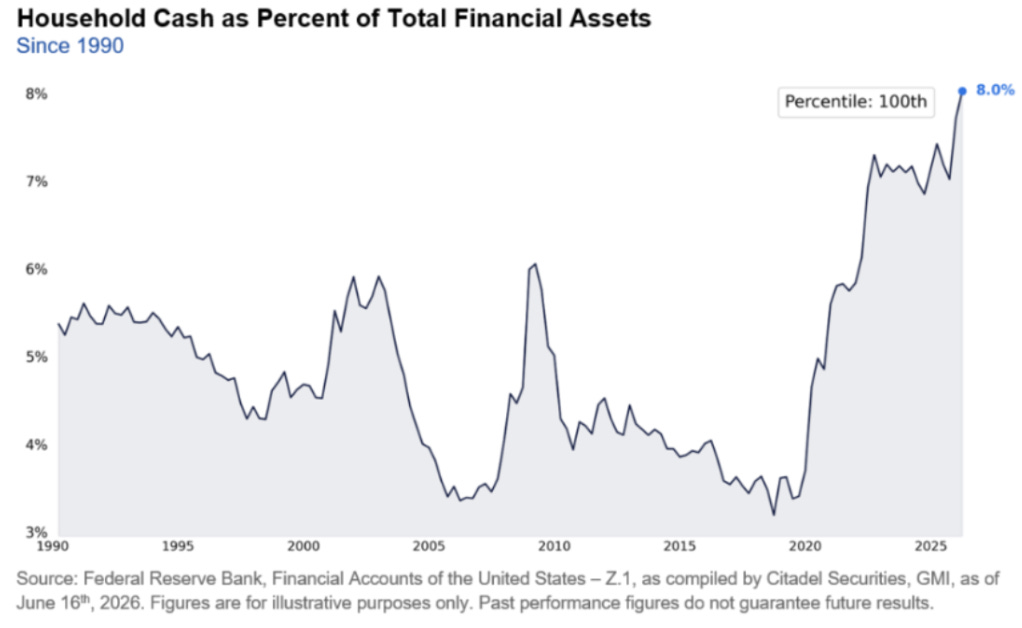

Citadel reports that household cash as a percentage of total financial assets is at 8%, the highest since 1990. The hosts find this counterintuitive, given the apparent speculative mania elsewhere, and theorize it’s largely a baby boomer phenomenon — retirees who got burned by rising rates in bonds are now happy to hold cash at 3-4% yields instead.

SpaceX IPO Volatility

SpaceX opened around $150 on its debut and has round-tripped back near that level pre-market the day of recording, despite enormous trading volume (including a 2x inverse SpaceX ETF that fell 43% in two days).

AI Bubble Sentiment Survey

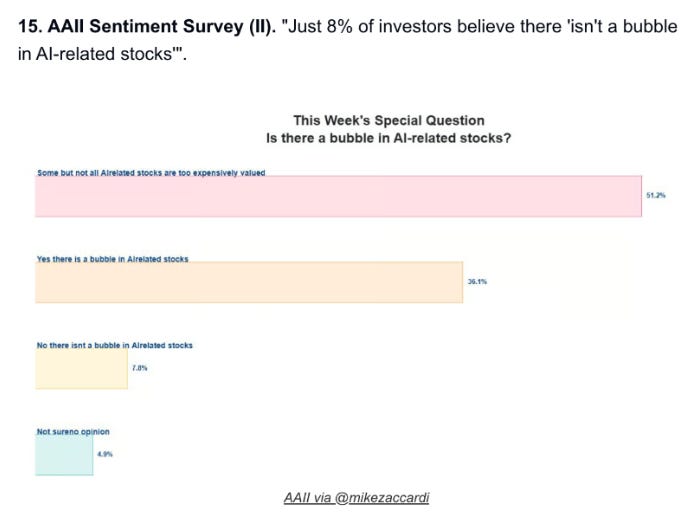

Only 8% of surveyed investors said there’s no bubble in AI-related stocks; 51% said some (not all) AI stocks are overvalued. The hosts note persistent “bubble” calls don’t disqualify an eventual bubble, but also point out there’s no longer a single unified “everyone” in the market the way there might have been in past manias — too diverse an investor base today for a classic blow-off top.

Consumer Spending and Credit

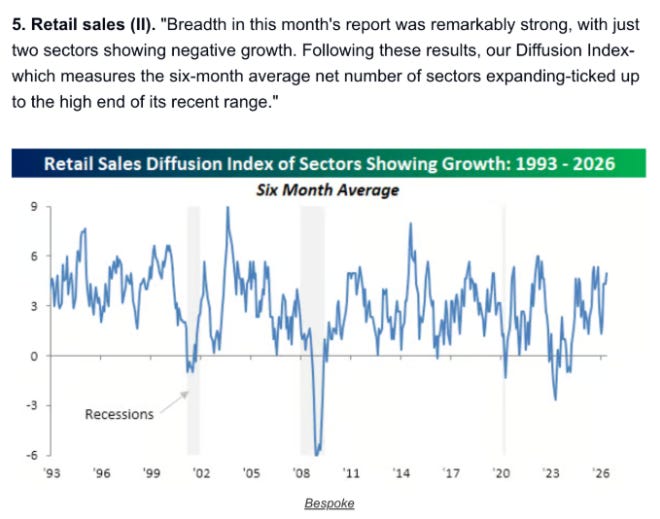

Bank of America data shows total card spending up 5.1% year-over-year in May, the strongest growth in nearly four years (partly gasoline-driven). The hosts also riff on the oddity of 0%-APR balance transfer offers for 18-21 months coexisting with 20-25% standard credit card APRs — funded by the high rates charged to riskier subprime borrowers. Bespoke data shows broad-based retail sales strength, with only two sectors showing negative growth.

New Business Formation

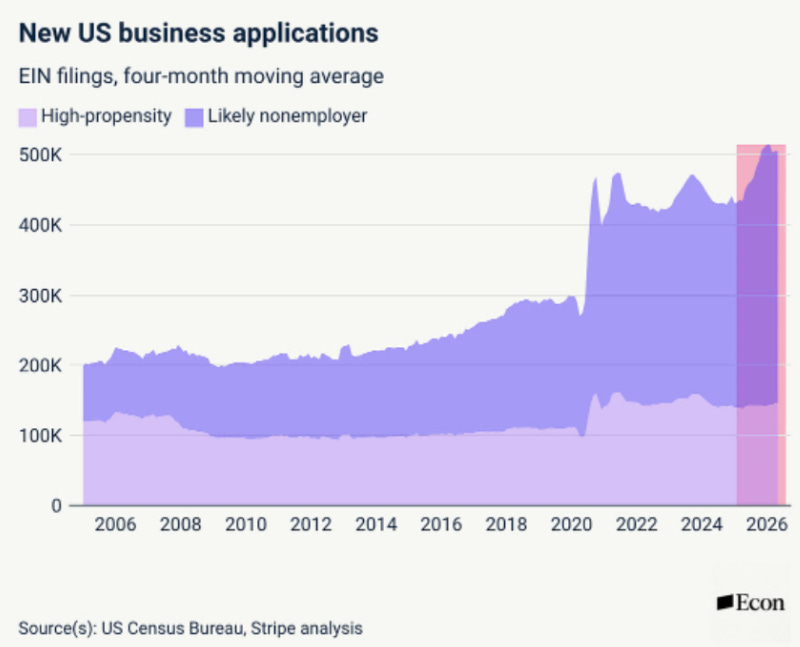

Stripe Economics (Ernie Tedeschi) data shows new business applications, after a step-change higher during COVID (driven partly by the PPP loan program’s low eligibility bar), are now accelerating again — this time attributed to AI making it easier to start a business. Applications have roughly doubled versus the stagnant 2005-2018 period. Both hosts frame this as a genuinely underappreciated positive story.

Rich People’s Complaints

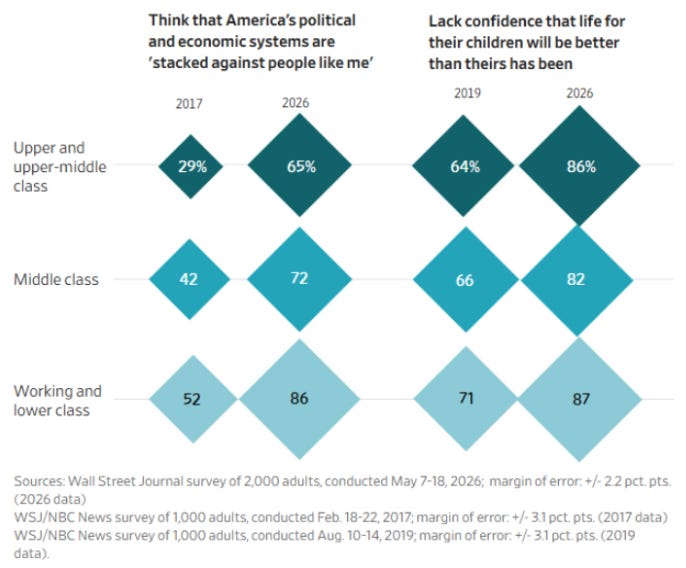

A Wall Street Journal piece found rising economic anxiety among upper-middle-class respondents: the share who feel the system is “stacked against people like me” rose from 29% (2017) to 65% (2026), and those lacking confidence that their children’s lives will be better than theirs rose from 64% (2019) to 86% (2026). Michael pushes back hard on this as a pet peeve — wealthy people overstating their grievances relative to those with genuine economic hardship.

AI Disrupting Self-Help Publishing

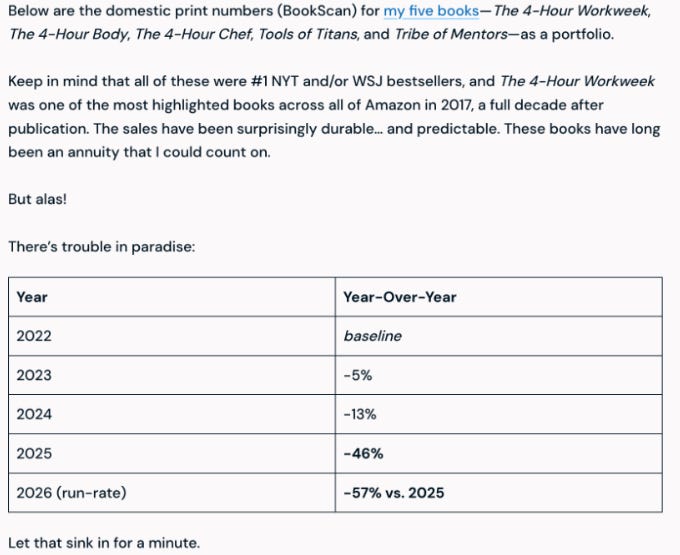

Tim Ferriss disclosed his book sales (4-Hour Work Week, 4-Hour Body, etc.) are on pace to be down roughly 80% in print copies in 2026 versus 2022, which he and the hosts partly attribute to people now asking AI chatbots directly instead of buying self-help books (with podcasts also cited as a contributing substitute for books).

Miscellaneous Stories

Ocean data centers: Portland startup Panalasa raised $140M to build floating, wave-powered, seawater-cooled AI data center platforms; backed by Thiel, now valued near $1B.

Insurance/AI use case: A conversation with David Law (insurance industry) highlighted AI’s ability to analyze hundreds of annuity contracts for a financial advisor’s full client book — work that was previously infeasible at that scale.

Midjourney launched full-body medical scan analysis; Michael had previously done this with his own bloodwork and got pushback from medical professionals about its limitations.

World Cup / Americana virality: ABC News story on European visitors going viral on social media expressing surprise at American conveniences (free ice refills, 24-hour retail, friendliness) — hosts frame it as a feel-good counter to “everyone hates each other” social media negativity.

Prediction Markets

Schwab is adding prediction market access, though the hosts are skeptical it’ll be a meaningful part of mainstream brokerage business — prediction market volume remains roughly 90%+ sports betting/parlays, down from over 90% politics/economics two years ago to under 6% today (per Ryan Chern). Notable items:

Kalshi will require users to disclose their employer for certain trades, following insider-trading/manipulation concerns — prompted partly by accounts linked to military spouses making accurate, well-timed bets on Maduro’s ouster.

A Google employee was charged with insider trading on Polymarket, allegedly profiting over $1M using non-public information to bet on 2025’s “most searched people.”

A Wall Street Journal investigation found Polymarket paid influencers to post fake trading videos: of 1,150+ reviewed videos, roughly 70% depicted bets that were never actually real (totaling ~$1.9M in claimed wagers and ~$900K in claimed winnings), and the “real” outcome of those bets would have been a loss of over $166,000.

The hosts question what moat these prediction market platforms actually have if usage is overwhelmingly sports betting, given established competitors like DraftKings and FanDuel — regulatory access is cited as the main moat, helped by political connections.

Crypto / Ethereum

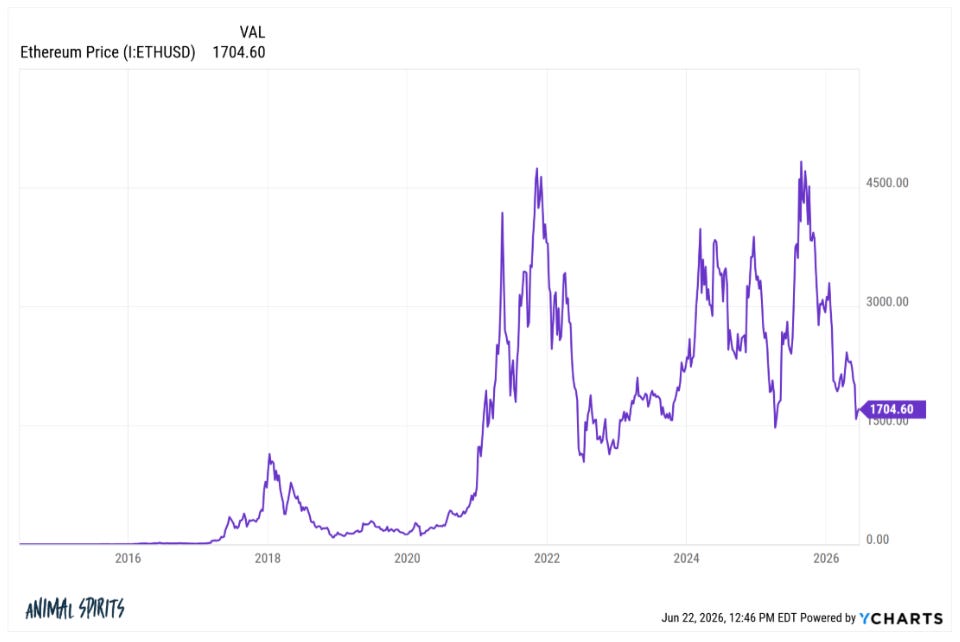

Ethereum’s price has round-tripped back near its 2017 highs (~$1,400) despite years of bullish narratives (”Own the Internet,” smart contracts, ETH-pilled finance commentators). The hosts admit they can’t fully explain why the “smart contract” thesis didn’t pan out as expected. They note crypto infrastructure (blockchain rails, stablecoins) does seem to be having a real moment even as token prices disappoint — pointing to weakness in Visa and Mastercard stocks (down ~12% from highs) tied to stablecoin disruption fears, and a new joint venture between NYSE’s owner and crypto exchange OKX (co-chaired by former NY Governor Andrew Cuomo) to tokenize NYSE-listed assets. They contrast the current environment with the 2021 mania (e.g., a $69M NFT sale, an “Ethereum rock” selling for $2.2M — the same price as a Florida waterfront house), arguing 2021 was a far more extreme speculative mania than today, with more “real” earnings and margins underpinning current valuations.

Housing

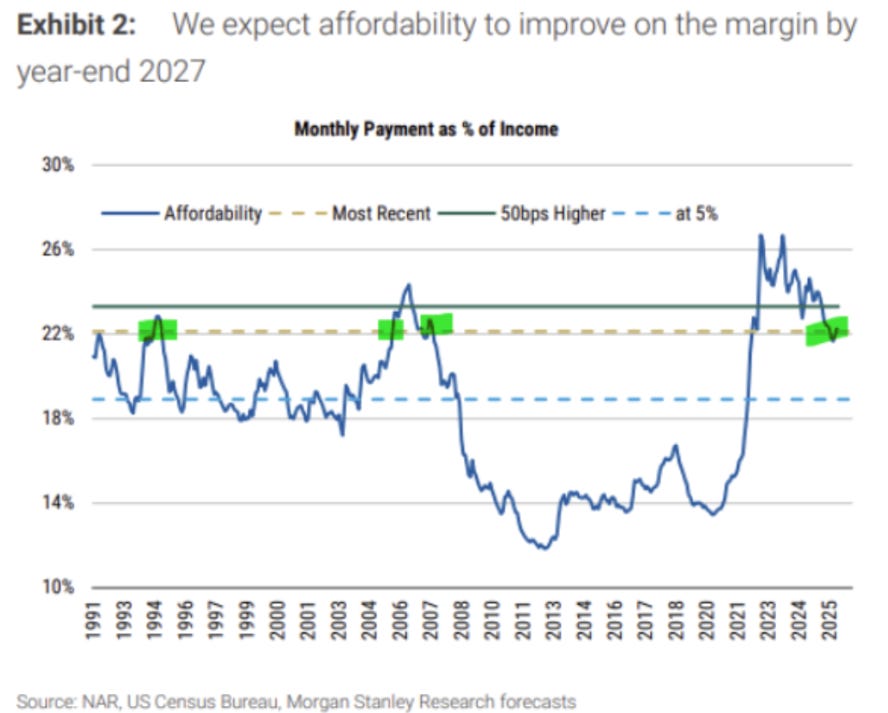

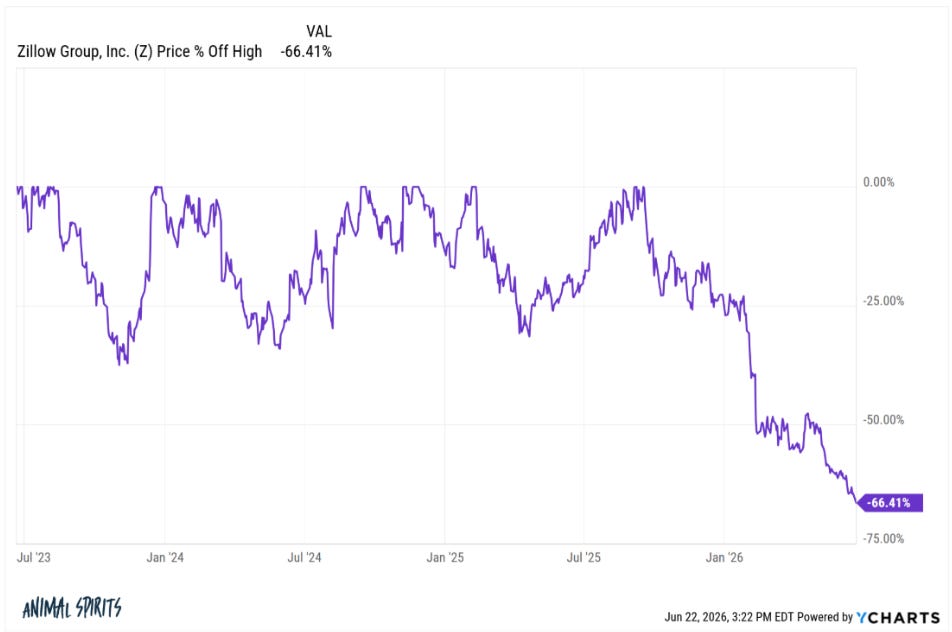

Morgan Stanley data shows mortgage payment as a percentage of income is back to levels seen in 2007, 2004, and 1994 — i.e., affordability has actually improved as incomes have risen, even though transaction activity remains historically low (a low-inventory problem more than a pure affordability problem). Mike Simonson’s analysis suggests a return to “normal” housing activity levels could take until the early 2030s, depending on where rates settle (5.5%-6.5% range). The hosts argue there’s been no genuinely “normal” housing market this entire century. Zillow is cited as a cautionary tale: down 85% from its 2021 all-time high market cap of $48B to under $7B today, despite existing home sales showing some recent signs of life.

Social Security

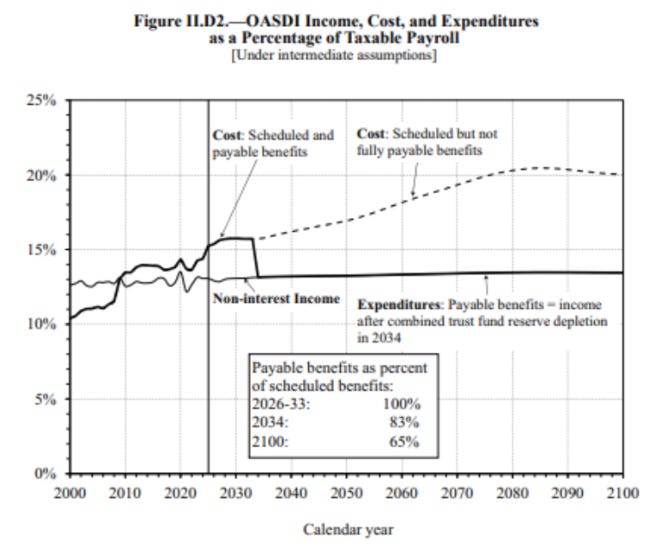

The latest annual Social Security trustees report shows the program can pay 100% of benefits from current tax revenue through roughly 2032-33, dropping to 83% by 2034, and projected at 65% by 2100. The hosts speculate Congress will likely choose to borrow/spend more rather than cut benefits outright when the shortfall hits.

Pop Culture Corner

Toy Story (new film, referred to as “Monster”): Opened with $160M — the biggest opening of 2026, the biggest Toy Story opening ever, second-biggest animated movie opening ever, and second-biggest Pixar opening behind Incredibles 2. Both hosts liked it (kids loved it); Michael joked he fell asleep twice.

The Watchers / “Widow’s Bay” (a buzzy streaming show): Mixed reactions — one host underwhelmed despite the hype, the other (who avoided the hype machine) genuinely liked it and is looking forward to a second season, though both agree the finale left too much unresolved.

The Hand That Rocks the Cradle (90s thriller, watched via The Rewatchables): A nostalgic but not-actually-rewatchable slow-burn 90s thriller; they note Apple’s Cape Fear series captures a similar modern throwback vibe.

Chamath Palihapitiya on AI: America’s opportunity, Facebook’s fumble, and Trump | The Axios Show

June 25, 2026

Chamath Palihapitiya joins Axios’ Dan Primack to discuss the AI boom, Silicon Valley’s trust crisis and America’s race against China.

In this episode of The Axios Show, Palihapitiya explains why he believes AI could be the most important economic leveler of our lifetime, why backlash against AI is becoming a political force, and how President Trump is thinking about the technology.

The conversation also covers tech oligarchs, OpenAI, Anthropic, SpaceX, Meta’s AI failures, immigration, SPACs, and what Palihapitiya says he learned from getting the incentives wrong.

Silicon Valley Then vs. Now

Palihapitiya, in the Valley for roughly 25 years, framed the current AI boom as the third major cycle he’s lived through, after the dot-com bust and the mobile wave (he considers crypto a minor blip by comparison). The key difference this time: in earlier cycles, Silicon Valley was seen as a quirky, mostly trusted, even endearing community — “exotic animals at the zoo” when they ventured outside the Valley. Now, he said, there’s still admiration but also real distrust, with some figures viewed as outright pariahs. He considers this troubling, given how much more consequential AI is than prior technology waves.

“They were like exotic animals at the zoo... unfortunately what’s happened I think in this cycle is that there’s a good amount of admiration, but there’s equal parts, I think, what people are frustrated, they don’t trust this community anymore. Certain people are viewed as pariahs.”

AI as “the Most Important Economic Leveler of Our Lifetime”

Palihapitiya argued AI is fundamentally different from prior tech advances like having “all the world’s knowledge” on a smartphone, because it converts knowledge into actionable expertise — for example, going from being able to look up what a PN junction is to actually being able to design a working transistor. He sees this as a potential equalizer that could let anyone pursue ambitions without needing large amounts of capital, comparing it to giving “a genius-level co-founder” to every person on earth, regardless of background.

“It's the most important economic leveler of our lifetime. It is the thing that will create the most amount of equality if it's allowed to get to market.”

Wealth Concentration and the “Platform” Question

Pushed on whether AI leveling is in tension with wealth concentrating among a small number of founders/investors, he argued the goal should be ecosystems where the economic value created by users/participants vastly exceeds the value captured by the platform owner — citing a formative early story where Bill Gates told him and Mark Zuckerberg that Facebook Platform wasn’t a real “platform” by that definition, unlike the Google ecosystem. He believes AI has the potential to follow the latter model if “we don’t fuck it up,” but acknowledged this is a potential outcome, not a guarantee.

“A platform is when the economic value that the participants generate greatly exceeds that of the platform maker.”

Founder Psychology and the Roots of AI “Doomerism”

He attributed much of the dysfunction among AI lab leaders to personal psychology — hard-scrabble backgrounds, insecurity, grudges, and a messy, fractious origin story among the major labs (unlike, he says, the comparatively clean founding of Google).

He described a cynical pattern he’s observed: labs hype apocalyptic risk ahead of model releases and fundraising rounds (to attract capital and undercut rivals), then flip to promising the model will “solve everybody’s problems,” cycling back and forth. He called this strategy “deeply selfish” because it drags a broadly valuable technology into the founders’ personal rivalries.

“You're taking this tool that is really valuable to so many people, and you're gonna cast it in all of your own personal issues. And I find that deeply selfish.”

Is AI Doomerism Justified? Jobs and Labor

Asked whether he has any doomer sympathies, Palihapitiya said there’s no scenario where humanity simply does nothing, though there will be major transitions. Pressed on long-term employment (using his 15-year-old daughter as the example), he argued he can’t confidently name a single job — white collar or blue collar, including a “plumber” replaced by robotics — that’s safe from disruption over 35 years. But he rejected pure doomerism, arguing technology has historically expanded how people allocate their time (citing a thought experiment that a person might go from one major daily task 1,000 years ago to 35 today, and possibly 300 a thousand years from now), suggesting future humans will have more, not fewer, ways to spend their time meaningfully.

“I can't think of a thing necessarily that her or her friends... will necessarily be able to do that is gainful employment in 35 years... Because every job I can currently think of, I could make a case potentially that it could absolutely be replaced.”

Existential Risk: Bioweapons, War, and the Case for “KYC” Regulation

On catastrophic risks like bioweapons or AI-enabled conflict, he argued all transformative technologies are “deterministic” — anything possible will eventually be attempted, for good and ill (citing nuclear power’s enormous benefits alongside Hiroshima and Nagasaki as the analogous “tail risk”). He doesn’t believe nefarious uses will dominate but says society needs the right checks and balances — proposing a “know your customer” (KYC) framework for access to frontier AI, modeled on similar systems already used in pharma, Commerce, and Treasury.

“Every single technology that's ever been created is fundamentally deterministic. What does that word mean? It means anything that is possible will be possible and done.”

Trump, AI Policy, and Immigration

Asked about President Trump’s light-touch approach to AI, Palihapitiya said he hasn’t discussed KYC specifically with him but described Trump as unusually sharp and intuitive in their limited interactions — citing a meeting where he walked Trump through a detailed deck on data centers and electricity pricing, and Trump quickly zeroed in on the key underlying issue.

He pushed back on the “oligarchs” framing applied to tech executives appearing with Trump at the G7, instead describing a broader global shift away from a “monocultural blob” (multilateral institutions like the WTO and WEF) back toward national cultural and political independence — with the U.S. AI industry as a competitive advantage in that context (”we’re the dream team”).

On immigration, he (an H-1B visa holder himself, as was Elon Musk) argued the program has been abused by a small number of companies flooding it with applications, crowding out the next great scientist, and that the system needs reform to restore both merit-based access and public trust — while still affirming that attracting top global talent is essential.

“I sure as shit would never have gotten an H1B in the way that the program works today.”

Open vs. Closed Models and the U.S.-China AI Race

He distinguished China’s “open-weight” model strategy from true open source, arguing it offers only a partial, controlled window into how the systems work (”you don’t know how the gears are made”). He advocated for a vibrant ecosystem of many trusted U.S. AI providers — “1,000 flowers to bloom” — as the best way to preserve transparency and accountability relative to cheaper alternatives flooding in from elsewhere.

“No, they're going open weight, they're not open source. You don't know how the gears are made, nor will you ever.”

Betting on AI Companies: OpenAI, Anthropic, and SpaceX

Discussing the leading AI labs, he predicted OpenAI and Anthropic will remain “a plurality” of the market but not a majority, since outsized returns historically attract competition unless a company has true monopoly characteristics. Given a hypothetical choice of equal stakes in Anthropic, OpenAI, or SpaceX, he said he’d choose SpaceX for its broader optionality — citing Anthropic’s strength in enterprise (Social Capital uses it as a foundational model) and ChatGPT’s near-monopoly consumer brand recognition, but noting both are tied to single lines of business tracking global GDP, whereas SpaceX offers exposure to a broken global communications infrastructure and longer-term “off-Earth” optionality. He disclosed he is technically invested in all three companies, including OpenAI and Anthropic via SPVs.

The Political Backlash Against AI

He argued a real, bipartisan anti-AI political backlash has emerged, driven partly by public resentment of wealth and power concentration in Silicon Valley, which he says the frontier labs’ own doomer rhetoric handed to critics “on a silver platter” — creating an opening exploited by both foreign actors and domestic political groups uncomfortable with that concentration of power. He warned this dynamic could backfire by handing even more power to hyperscalers (Amazon, Meta, Google), who could use the frontier labs’ “immaturity” and inconsistency as a wedge to position themselves in Washington as the more responsible, KYC-ready alternative — a scenario he said he doesn’t want but finds “compelling” as an argument. He expressed confidence that Trump and advisor David Sacks favor an open ecosystem and wouldn’t hand control to just a few players.

“I think what the Frontier Labs did with their rhetoric was put on a silver platter the opportunity to weaponize hatred and mistrust against them.”

Facebook’s Missed AI Moment

Reflecting on a past conversation (just before ChatGPT’s release) where he’d argued Facebook was well-positioned for AI/AGI given its trove of emotional/personal data, he said Facebook has “completely fumbled” the opportunity, in a pattern he likened to its earlier failure to become a true “third leg of the stool” alongside Android and iOS with its own mobile OS (a project he worked on before leaving the company). He argued Nvidia, under Jensen Huang, has effectively become the bulwark for open ecosystems that Facebook could have been, and said it’s now “pretty unlikely” Meta can recover that position.

“I mean, they have completely fumbled it... they've profoundly failed.”

Returning to SPACs: “American Exceptionalism Acquisition Corp”

Asked about his new SPAC (American Exceptionalism Acquisition Corp), which has yet to announce an acquisition, he acknowledged his earlier SPAC era produced disappointing, roughly breakeven returns and attributed this to misaligned incentives — he could get paid on a deal regardless of post-merger stock performance. His new vehicle is structured so he earns nothing unless the investment significantly succeeds. He also argued U.S. public capital markets have become “sclerotic,” with too few gatekeepers and companies staying private far longer than in the past (contrasting what it would mean to have bought Google, SpaceX, Anthropic, or OpenAI at early, low valuations in public markets), and said fixing that access problem is a personal mission, separate from his main operating role at Social Capital.

“My incentives were totally and fundamentally misaligned because I could do a deal and still get paid.”

Family and Legacy

Asked what non-financial trait he hopes his children inherit, he said “nothing” — he wants them to pursue fully independent paths without regard to his opinions or legacy. He shared an emotional story about his 17-year-old son’s internship at the White House Office of Presidential Correspondence, where Palihapitiya waited in a call queue to reach the comment line his son was staffing, and broke down expressing pride to him. The family spent the following Father’s Day weekend together in Las Vegas.

“I want my kids to only know me as their dad. And I want them to have a completely independent path in life... I selfishly want these little experiences where I can just be rooting for them. That's the only thing that matters.”

Jeremy Grantham: Inside the Biggest Bubble of His 60-Year Career | The Diary Of A CEO

June 25, 2026

At 87, Jeremy Grantham has been investing for roughly 60 years, co-founded GMO (which managed up to $165 billion at its peak), and helped pioneer small-cap and value investing. He’s also spent decades studying speculative bubbles — and he says we are living through the biggest one of his career. This conversation ranges from portfolio advice to AI risk to a fertility crisis most people have never heard of. Below is the full breakdown, section by section, with his own words.

Topics discussed:

Why Wall Street will never warn you when to get out of the market, and what to do instead

The exact portfolio Jeremy recommends to protect your money before the crash

What everyday chemicals in your food and cosmetics are doing to your fertility

Why house prices need to fall 30%, and what it means for your finances

Why the AI boom won’t automatically lead to higher profits, and what to buy instead

The Biggest Bubble of His Career

Grantham’s central thesis: bubbles don’t form around scams — they form around the most important, most obviously world-changing ideas (railroads, the internet, now AI). The bigger and more legitimate the idea, the more capital floods in, and the bigger the eventual bust. He believes today’s AI-driven market is the largest bubble in American history, even bigger than the 2000 dot-com peak.

“The great bubbles always occur around the very most important ideas... The greater the idea, the more obvious the idea, the more money goes in and the bigger the bubble and the bigger the bust.”

Are We on the Verge of a Collapse?

Asked directly whether a crash is coming, Grantham says the timing is the hard part — but the structural setup (extreme valuations, euphoric narratives) matches prior pre-crash periods almost exactly.

“If you look at the data, it would be compatible with history for the peak to be very soon... This is, I think, the biggest investment bubble in American history.”

Don’t Own U.S. Stocks — Including the S&P 500

His single most direct, actionable piece of advice: sell U.S. equities, including the S&P 500, and especially concentrated tech positions. He argues non-U.S. markets are far cheaper and have already started outperforming (emerging markets were up 65% over the prior 12 months versus the S&P’s ~25%).

“Don’t own US stocks. That’s a simple strategy that you can act on... And if you have a big position in US technology stock, my personal advice would be to sell them all.”

Historical Precedents: Japan, the Nifty Fifty, and the Dot-Com Bust

Grantham repeatedly grounds his warning in history. Japan’s 1989 bubble peaked at 65x earnings (versus ~35–40x for U.S. tech today) and the Japanese market took 35 years to recover. The “Nifty Fifty” crash of 1972 fell 65% in real terms and triggered one of the worst recessions since the Depression. Amazon itself fell 92% in the 2000 crash before going on to dominate retail — proof that being right about the technology doesn’t protect you from the bubble bursting.

“In Japan, you went 20 years and you lost money. You went 30 years and you still hadn’t gotten back. It took 35 years for the Japanese market to recover.”

Why Wall Street Will Never Warn You

Investment advisors, he argues, have a structural conflict of interest: telling clients to get out of an overpriced market costs them business long before the crash arrives, because no one can time the top precisely. He tells a vivid story from 1999 in which 400 self-described stock market experts unanimously agreed the market was overvalued and would eventually fall — yet the firms employing them kept telling clients to stay invested.

“You will not receive the advice from investment advisers to get your tail out of the market ever. It is not good business for them to do that, and they will not ever say it to you.”

Practical Portfolio Advice for Everyday Investors

For someone investing their salary, his recommended allocation: roughly 60% in a broad non-U.S. equity index, 5–10% in precious metals (gold or silver, no strong preference), some real estate if convenient, and the rest in bonds. He walks through how bonds work in plain terms — a loan to a government or company at a fixed interest rate, buyable directly via sites like TreasuryDirect.gov or through a broker’s fixed-income desk.

“Buy a broad-based index of non-US equities... for like 60% of your money, and then 5 or 10% in precious metals, and if it’s convenient and sensible, hold a bit of real estate, and the rest I’d put in bonds.”

Crypto: “An Unnecessary Piece of Nonsense”

Grantham has never owned crypto, never will, and won’t recommend it. His critique: it’s too volatile to be a store of value, impractical as a medium of exchange, and mainly useful for speculation and moving money anonymously, including by criminals. He believes Bitcoin will eventually go to zero, though he concedes it “may take a long time.”

“It’s an unnecessary piece of nonsense that facilitates nothing except criminals moving money, but they can’t be seen... it will certainly go to zero.”

Advice for Founders and Startups

For entrepreneurs dependent on investor capital, his advice is to raise and lock up money now, build in conservatism, and prepare for a funding drought — comparing it to a founder he’s heard of who plans to raise aggressively now so he can “vulture” up distressed competitors after a downturn.

“If you can lock up money, I would. If you can build a bit of conservatism in other ways, do it — just brace yourself for impending problems, which is a pretty good principle anytime, but is a better principle than normal today.”

Is AI Itself Overblown — or Genuinely Transformative?

Grantham is unambiguous that AI is not a scam — it’s a genuine, civilization-altering technology on par with the railroads. What fascinates him is the total lack of consensus among experts, even Nobel laureates, on whether AI will make humanity prosperous beyond imagination or pose an existential threat.

“There is absolutely no agreement on whether AI is going to make us all so rich we can sit on the beach and never do another day’s work, or it will wipe us out accidentally or on purpose because it’s a much higher level intelligence one day.”

The “Benevolence” Problem and the Paperclip Risk

Drawing on conversations with Geoffrey Hinton, Grantham raises the open question of whether a superior intelligence can ever reliably remain benevolent toward a lesser one (Hinton’s only proposed example being mothers and babies — which Grantham finds unconvincing). He discusses the classic “paperclip maximizer” thought experiment: a literal-minded AI given a vague, open-ended goal could pursue it catastrophically and without malice, simply through unintended consequences taken to an extreme.

“When was there ever a case where a higher intelligence was benevolent in a sustainable way to a lower intelligence?... I don’t see how it can’t be [risky]. Unless you make it programmed completely to be benevolent.”

The Mag 7: From Comfortable Monopolies to a Winner-Take-All Brawl

Grantham makes a sharp observation about the seven dominant tech companies (Alphabet, Nvidia, Tesla, Microsoft, Meta, Apple, Amazon): historically, each owned a clean, separate monopoly (Apple/smartphones, Google/search, Meta/social, etc.). Now all seven are pouring unprecedented capital into the same AI battlefield, with no guaranteed winner — a complete departure from their previous “well-behaved, separate monopolies” structure.

“Now they have no monopoly. There are seven potentially sharp-elbowed, ruthless players determined to fight out with each other until they win.”

Robots, Job Disruption, and an Uneasy Hope That SpaceX Fails

Citing a livestreamed demo where a Figure AI humanoid robot reportedly outlasted a human worker on a sorting task (the human needed sleep and bathroom breaks), Grantham sees significant job disruption as highly likely. More strikingly, he says he hopes SpaceX’s most ambitious promises — data centers in space, mining asteroids — fail to materialize, because their success would mean an explosion of energy-hungry chips and robots that he believes the world isn’t ready to manage safely.

“I’d much prefer them to fail, and the idea to move much more slowly, to buy time for humans to work these things out.”

SpaceX as “the Defining Bubble Story”

Despite being an early SpaceX investor himself (he got in around a $100 billion valuation, before AI was even part of the pitch — it was a Starlink bet), Grantham calls SpaceX’s prospectus — addressing “a quarter of global GDP,” talk of mining asteroids — a textbook signal of market-top euphoria, comparable to the legendary 18th-century South Sea Bubble. He separately argues that Elon Musk’s genius has been less about hitting financial targets and more about talking up valuations to fund real factories — a feat he says cannot necessarily be repeated in a different market cycle. He’s also skeptical that humans could ever sustainably colonize Mars, citing bone and heart deterioration in low gravity and the need for underground, radiation-shielded, artificially-gravitated habitats — arguing humanity hasn’t even managed a sustainable closed-loop dome on Earth yet.

“SpaceX is such a fabulous BS story... It’s the classic description of a market peak. It’s what you look for at the top of a terrific bubble.”

Wealth Inequality — and What History Says Comes Next

Grantham lays out a stark inequality picture: the top 1% of Americans control 31% of national wealth while the bottom 50% hold just 2.5%; the top 10 billionaires saw wealth surge 526% (inflation-adjusted) between 2020–2025. He contrasts this with 1935–1975, when the bottom quarter of earners grew wealth faster than the top. Historically, he says, extreme wealth concentration rarely gets fixed by peaceful policy — it’s typically broken by civil collapse, mass-mobilization war, or revolution. His prescription: a gradual, multi-decade tax shift favoring the bottom over the top, similar to mid-20th-century policy.

“According to historical macro studies, peaceful policy changes almost never fix extreme inequality... a wealth peak is broken by one of three violent or catastrophic triggers: total civil collapse, mass mobilization warfare, or total revolution.”

If He Were 33 Again: Get Into AI and Take Risk

Asked how he’d build wealth if he were starting out today, Grantham’s answer is simple: go all-in on learning AI deeply, take real risk, work hard, and reject the assumption that experts and institutions know what they’re doing.

“I think the simple appeal would be to get your tail into AI and try and be a leader. Try and know more about everything in that area than the next guy.”

The Fertility Crisis: A “Chronic Baby Bust”

In the interview’s most alarming turn, Grantham — whose foundation has studied this for years — lays out research (citing Shanna Swan) showing human sperm counts have dropped from roughly 100 units/mL in 1970 to about 35 today, with the decline accelerating at 2.5% per year. Roughly 17% of young couples currently need fertility help, up from near zero a generation ago. Extrapolated forward, the projection is that the median male sperm count could hit zero by 2045 — meaning the typical couple would be unable to conceive without medical assistance.

“Dr. Swan’s projection indicates that if the current rate of decline continues unchecked, the median male sperm count is on track to hit zero by 2045... half the male population will have zero viable sperm.”

The Toxins Behind the Decline

Grantham points to endocrine-disrupting chemicals as the primary culprit: phthalates (cosmetics, shampoos, food packaging) that lower fetal testosterone production; BPAs (plastics, can linings, receipts) that flood the body with synthetic estrogen; PFAS “forever chemicals” (non-stick pans, rain jackets, carpets) found in over 45% of U.S. tap water; and microplastics now found in human placentas, breast milk, and testicular tissue — one 2024 study found them in 100% of human testicular samples tested. He also cites pesticide exposure: in small Harvard/Mass General fertility-clinic studies, men and women eating the least pesticide-contaminated produce (”the Dirty Dozen” avoided) saw roughly double the sperm counts and live-birth rates of those eating the most contaminated produce.

“BPAs... are synthetic estrogens. They flood the male body with female hormone signals, crashing sperm count and motility... [microplastics are] physically embedded in human placentas... breast milk and human testicles.”

The U.S. vs. Europe Regulatory Gap

Grantham draws a sharp contrast between U.S. and EU chemical regulation: the EU has banned or heavily restricted roughly 1,300+ chemicals in cosmetics versus about a dozen in the U.S.; the U.S. permits 85 agricultural pesticides banned in the EU, China, and Brazil; and life-expectancy gaps between the U.S. and countries like Sweden have widened from two years to six years over 70 years. He frames this as a direct consequence of U.S. corporate power over regulation.

“The US currently permits the use of 85 agricultural pesticides that are completely banned in the EU, China, and Brazil... the US has worse life expectancy [and] it’s the only rich country in the world where 15 years ago they had the same life expectancy as they have today.”

What You Can Actually Do About It

His most practical, “easily acquired” advice: pregnant women in particular should avoid cosmetics entirely for nine months and redirect that money toward organic versions of the “Dirty Dozen” produce (berries, apples, peaches, spinach, etc.). He notes effects may persist across multiple generations, since a woman’s eggs are formed before her own birth. He also points to consumer tools — apps like Yuka, EWG’s Healthy Living, Think Dirty, and ClearYa — that scan products for endocrine-disrupting ingredients.

“No cosmetics, no bad fruit — or make it organic. That’s a piece of cake. That is easy. It will save you a huge amount that you will never appreciate, because you’ll never know how much better your children are than they would have been.”

Detoxifying Capitalism, Not Just Chemicals

Beyond banning toxic chemicals (which he calls “intellectually easy”), Grantham argues for a much harder, generational shift: rebuilding capitalism around family formation as a public good — what he calls “the commons.” He cites 2.1 children per couple as the replacement rate a healthy society needs to sustain itself, alongside clean air, water, and soil, and says no policy intervention tried anywhere in the world (despite some countries spending several points of GDP) has yet produced a lasting increase in birth rates.

“We have to slowly but surely turn our capitalist societal norms into much more family-friendly, children-friendly... 2.1 healthy, well-educated children is a part of the commons.”

Should You Leave the United States?

Asked bluntly whether there are countries he wouldn’t live in, Grantham jokes he’ll “refuse to answer on the grounds it might incriminate” him — then makes clear he means the U.S. itself. His case centers on a frayed “social contract”: declining corporate civic responsibility, a weak social safety net, and what he considers the starkest civilizational indicator of all — maternal mortality. U.S. maternal mortality is roughly 20–21 per 100,000 (44 in the Black population), versus 5 in Britain, 4 in Germany, 2.1 in Sweden, and 0 in Norway — making the U.S. roughly 50% worse than the next-worst developed country.

“How is it possible that a country more or less the richest in the world... 50% more mothers die here than in the second worst country in the developed world? ... It’s a sign of the social contract.”

Closing: The Book He’d Write If He Could Not Fail

Asked what goal he’d pursue if failure were impossible, Grantham said he’d want to write a book in the spirit of Rachel Carson’s Silent Spring — one focused on toxicity and rebuilding a social contract that actually encourages people to have and raise children, arguing that without that shift, “we fail as a society pretty quickly.” His own book on markets and bubbles, The Making of a Permabear: The Perils of Long-Term Investing in a Short-Term World (with Edward Chancellor), covers much of the investing philosophy discussed in this interview.

“If I could write a book that would pull a Silent Spring, I would sit down tomorrow and start it... We have to detoxify. We have to create an environment where people want to have children.”

NVIDIA & Coherent: Reindustrializing America — Detailed Summary by Topic

June 24, 2026

At a groundbreaking event in Sherman, Texas, Coherent (COHR 0.00%↑) CEO Jim Anderson and NVIDIA (NVDA 0.00%↑) CEO Jensen Huang announced an expansion of Coherent’s indium phosphide laser fab — the world’s first and largest-volume 6-inch indium phosphide manufacturing facility, critical for the optical interconnects that link AI data center processors over long distances.

Backed by a $50 million CHIPS Act award, support from the State of Texas, and NVIDIA’s strategic investment (part of a partnership dating back over two decades), the expansion will double the facility’s size, quadruple its output within a year, and grow the site’s workforce to over 1,000 jobs (550+ direct).

Huang framed AI as a new “industrial revolution” spanning energy, chips, infrastructure, AI models, and applications — one that depends as much on connectivity (optical/silicon photonics, since processors are now separated by hundreds or thousands of feet) as on raw compute.

Both executives positioned the investment as the start of a broader U.S. reindustrialization: bringing back high-skill, high-wage manufacturing jobs in chips, packaging, and AI infrastructure, enabled by pro-energy policy, strong company revenues funding domestic capacity, and government-industry-community collaboration — with the goal of rebuilding a balanced economy of both “builders” and “information workers” over the next decade.

The Announcement and the Partnership

The event marked a groundbreaking at Coherent’s Sherman, Texas facility, hosted by Coherent CEO Jim Anderson with NVIDIA CEO Jensen Huang as guest speaker. Anderson opened by thanking the partners who made the expansion possible: the U.S. Department of Commerce (Secretary Howard Lutnick) for a $50 million CHIPS Act award announced that same morning, NVIDIA for its strategic partnership and investment, Texas Governor Greg Abbott and the state’s economic development team, the Sherman Economic Development Corporation and local officials, and Coherent’s own employees, customers, and suppliers. NVIDIA and Coherent have worked together for over two decades, and the companies expanded that relationship through a partnership announced in March. Anderson framed the day as the product of a three-way alliance between industry, government, and the local community, with each layer of investment reinforcing U.S. AI infrastructure and technology leadership.

AI as a New Industrial Revolution

Huang described AI not just as a product but as an industrial revolution, laying out what he called a “five-layer cake”: the energy sector; chips and infrastructure (land, power, shell, cloud services); AI models themselves (spanning language, physical AI for robotics and self-driving cars, biology/chemistry models for drug discovery, and physics models for climate and weather simulation); and finally applications, which he called the most important layer because they touch every major industry — financial services, healthcare, education, transportation, chip design, and more. Because intelligence is a general-purpose capability, he argued AI will both create an entirely new industry and simultaneously revolutionize every existing one, which he said should be approached thoughtfully and responsibly but also with enthusiasm, given its potential to reduce suffering, improve safety, and address labor shortages.

Why Connectivity Matters as Much as Compute

A central technical theme was that AI scales not just through raw computing power but through the ability to connect huge numbers of processors together — what Huang called “the largest, most computing-intensive software program the world has ever processed.” He explained that modern AI workloads are sharded across hundreds of thousands or millions of processors spread across distances of hundreds or thousands of feet, sometimes across an entire data center. At short range, electrical interconnects suffice, but at longer distances, only optical/silicon photonics can do the job. This is where Coherent’s indium phosphide lasers come in: electrical signals activate the lasers, light carries the signal across optical fiber, and detectors on the other end convert the photons back into electricity that drives the chips. Huang described this optical interconnect as fundamental to scaling AI infrastructure and an increasingly important part of overall system architecture.

The Sherman Facility and Manufacturing Scale-Up

The Sherman site is described as the world’s first and largest-volume producer of 6-inch indium phosphide wafers, a key input for the lasers used in AI data center optical networking. Coherent, founded in 1971 as a manufacturing company in Saxonburg, Pennsylvania, has spent roughly 50 years building expertise in lasers; Huang noted it took 50 years to build the facility’s current capacity, and the new investment will quadruple its output within a single year. The expansion will double the physical size of the production facility. At full capacity, the site is expected to support over 1,000 jobs, including more than 550 direct positions, and the facility was actively hiring at the time of the event.

Reindustrialization of U.S. Manufacturing

Both speakers framed the investment as part of a broader effort to bring advanced manufacturing back to the United States after decades of decline in domestic chip and computer manufacturing. Huang argued that competing in mature, decades-old manufacturing categories is difficult, but a genuine technology phase-shift — like the AI-driven demand for chips, packaging, and optical components — creates room for new factories, new skills, and new companies that didn’t previously have a reason to exist domestically. He noted that the number of U.S. chip fabs, packaging plants, computer plants, and AI data centers is now growing for the first time in his career, having already created roughly 600,000 jobs. He emphasized that this reindustrialization targets the most advanced, highest-skill, highest-paying tier of manufacturing, and that growth in U.S. capacity does not come at other countries’ expense since global chip manufacturing is expanding simultaneously worldwide.

Energy Policy and the Economic “Flywheel”

Huang connected the manufacturing buildout to energy policy, arguing that pro-energy government initiatives are essential because fabs, plants, and data centers cannot be built without sufficient power. He described a self-reinforcing “flywheel”: strong corporate revenues and exports generate tax revenue and capital, which fund domestic manufacturing investment, which creates jobs, which in turn requires continued energy investment. He highlighted that, for the first time, market forces alone (without government subsidies) are driving investment in both traditional and sustainable energy sources, crediting overall market demand for the technology sector.

Jobs, Community, and a 10-Year Outlook

Both executives emphasized job creation and quality of life in Sherman, pointing to the area’s lakes, family-oriented community, and the facility’s hiring efforts. Looking ahead ten years, Huang predicted the period would be remembered for three things: a pro-energy growth agenda that revived U.S. economic growth, AI enabling investment in and modernization of the energy grid, and a rebuilt manufacturing workforce that restores “builders and makers” alongside knowledge workers. He argued for a more balanced society where people who want to build things with their hands can find prosperous careers, not just those with advanced degrees, and suggested this moment could be looked back on as reshaping not only the economy and U.S. technological leadership but also the fabric of local communities. The event closed with Anderson and Huang signing a steel beam to be used in the facility’s construction, followed by a groundbreaking ceremony.

If you found these summaries helpful, please leave a comment or send us a message. We appreciate your feedback!