From Chips to Power Grids. The Hidden Bottlenecks Behind the AI Gold Rush

Lesson 2. Analysis of the AI investment surge, supply chain and infrastructure bottlenecks, and evolving funding models.

Lesson 2 of The Economics of AI covers the capital investments companies are making to build out AI infrastructure, how they compare with other mature industries, and the bottlenecks that prevent us from realizing the full potential and benefits of Generative AI innovations.

Find all the lessons in The Economics of AI here and the previous lesson below.

Lesson 1: How Technology Platform Shifts Reshape the World

Every decade or so, we see the emergence of a new technology that changes how we develop tools, solve problems, and organize ourselves. Generative AI is just one such technology shift people have lived through, and one of many we are currently living through. We will cover what historically happens in a technology shift and the impact we can expect to see in the tech industry and beyond.

The Capital Tsunami: Analyzing the AI Investment Surge

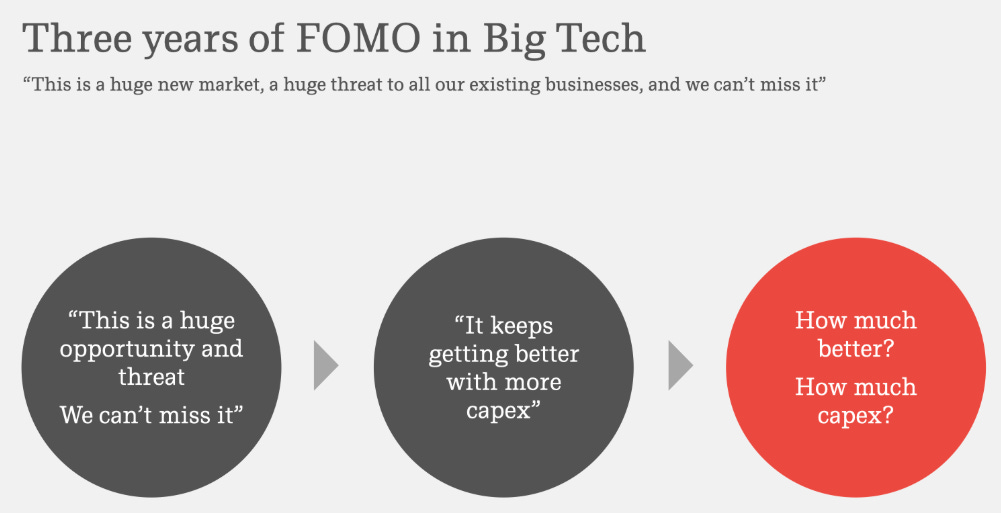

The fundamental uncertainty surrounding AI’s ultimate potential has triggered a capital expenditure (capex) boom of historic proportions. This ambiguity is the primary psychological driver of the intense FOMO (Fear Of Missing Out) gripping the world’s largest technology companies1.

The prevailing sentiment, as articulated by Google CEO Sundar Pichai

“The risk of under-investing is significantly greater than the risk of over-investing.”

and Meta CEO Mark Zuckerberg

“The very worst case would be that we have just pre-built for a couple of years.”

This mindset has unleashed a torrent of capital aimed at building the foundational infrastructure for the AI era.

The Scale of Investment

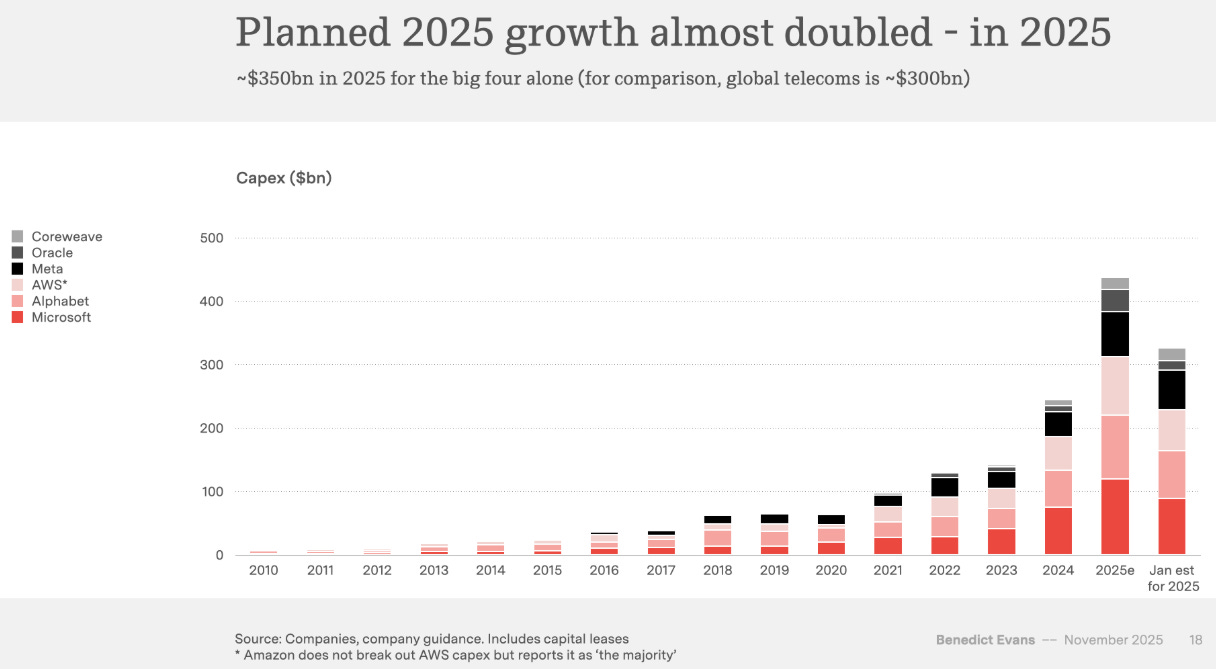

The numbers behind this investment surge are staggering. The four largest platform companies are on track to spend nearly $350 billion on infrastructure in 2025 alone, a fourfold increase from just a few years ago.

This spending is expected to accelerate, with Microsoft, Alphabet, and Meta signaling that their capex growth rates in fiscal year 2026 will be even higher than in 2025.

“We now expect the FY26 growth rate to be higher than FY25” - Microsoft

“Capex dollar growth will be notably larger in 2026”- Meta

“We expct a significant increase in 2026” - Alphabet

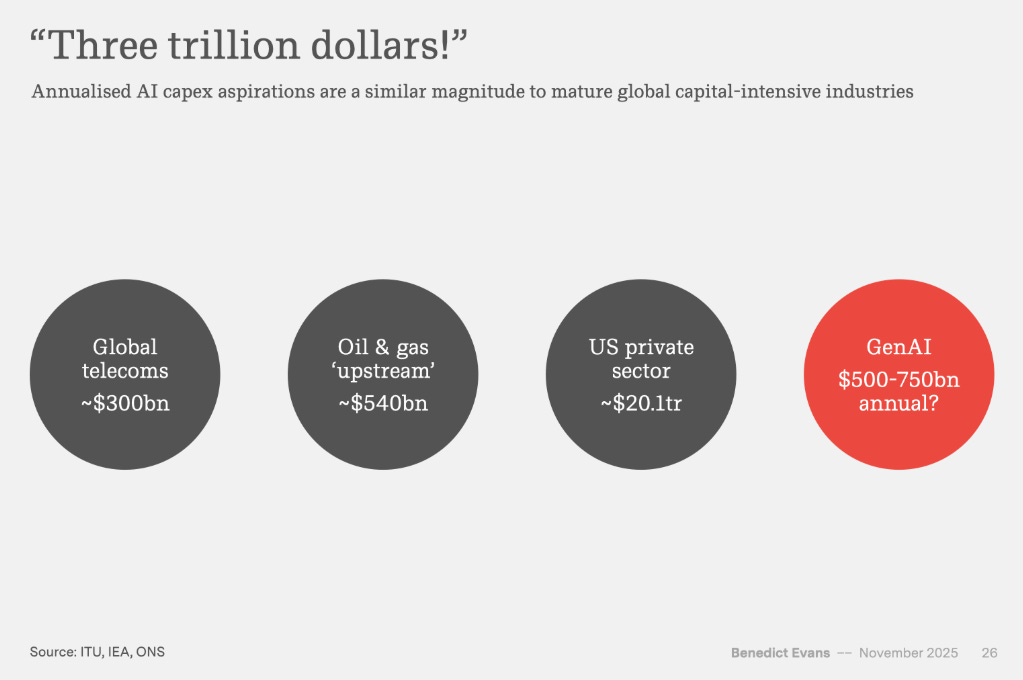

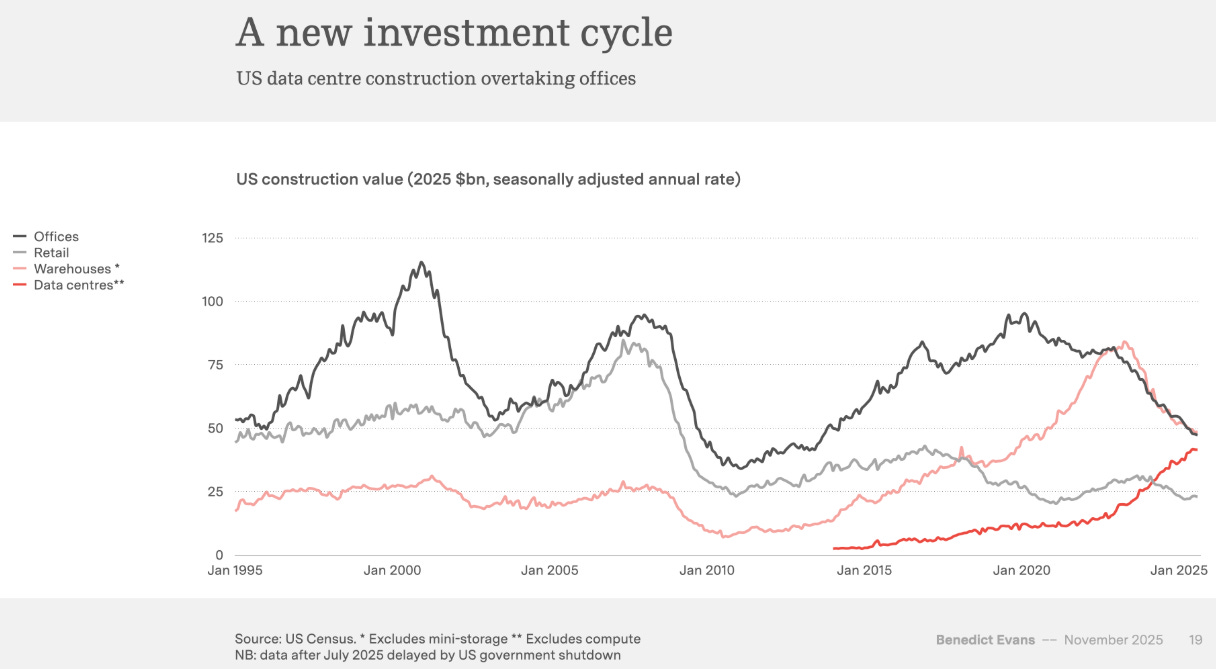

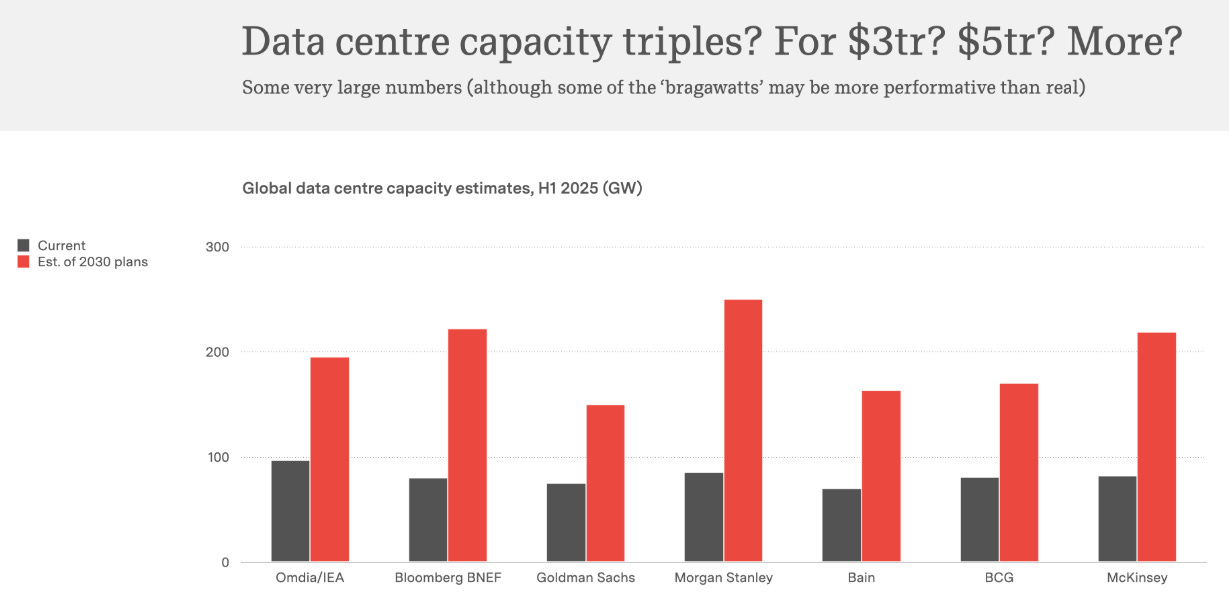

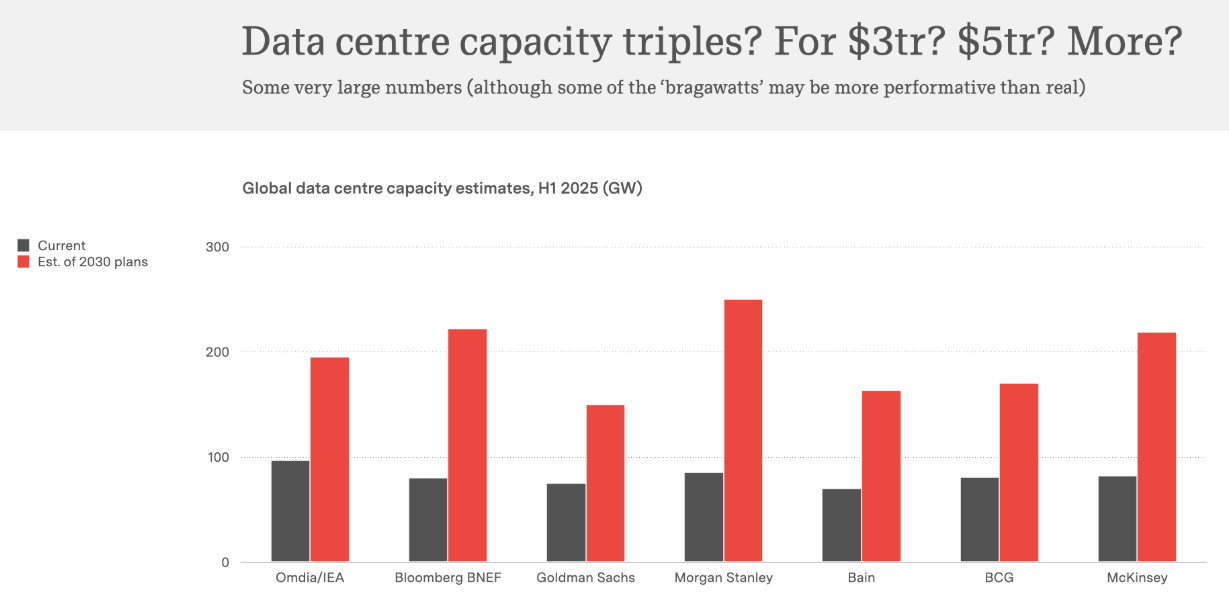

To put these figures in perspective, the potential annualized capex for generative AI infrastructure, estimated at $500-750 billion, would rival or exceed the spending of entire global capital-intensive industries, such as telecommunications (~$300 billion annually) and upstream oil and gas (~$540 billion annually). The value of data center construction will soon overtake that of office and warehouse construction.

Supply Chain and Infrastructure Bottlenecks

This unprecedented demand is placing immense strain on the global technology supply chain, creating significant bottlenecks that constrain the pace of deployment.

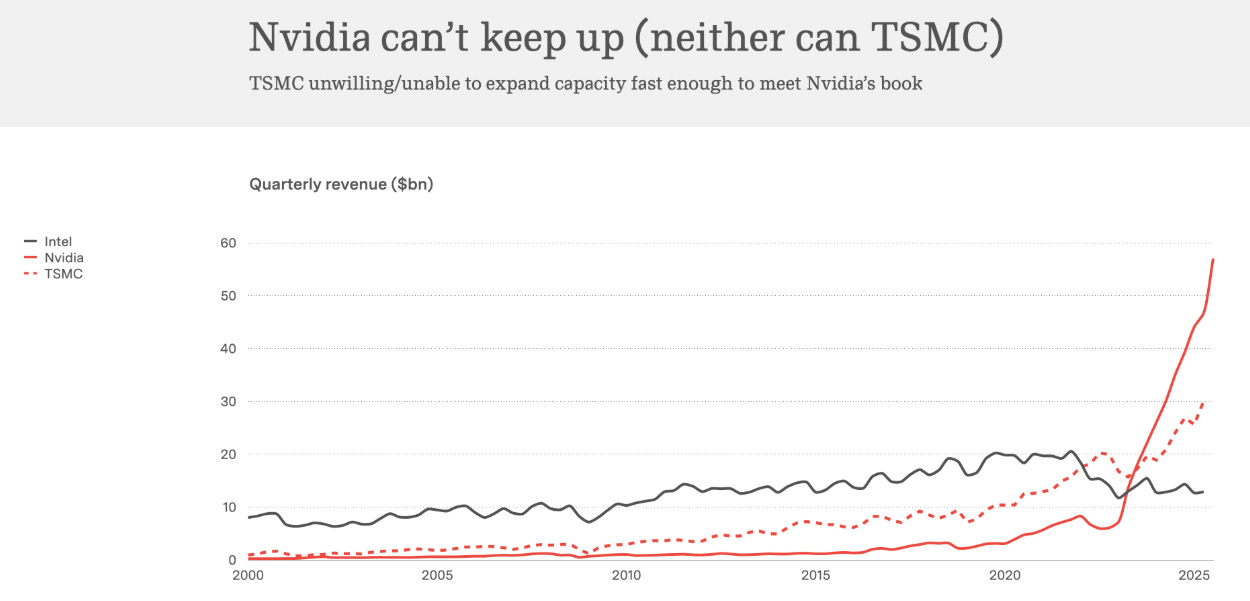

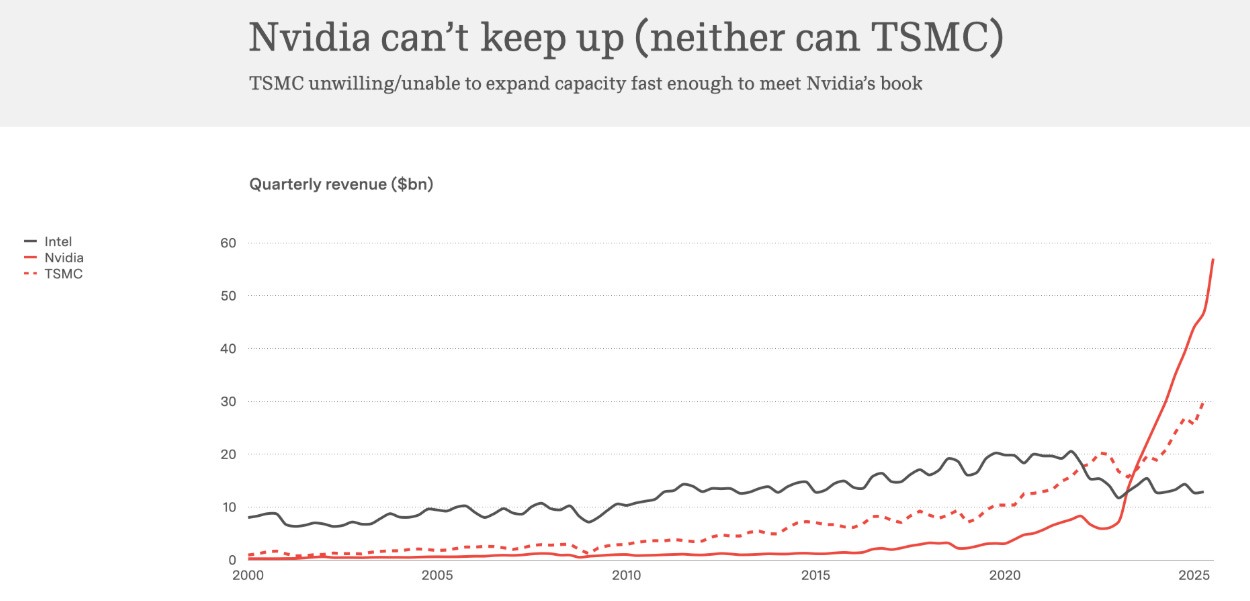

Chips: Nvidia, the dominant provider of AI chips, “can’t keep up” with demand, reporting a quarterly revenue run rate of $40 to $50 billion. Its manufacturing partner, TSMC, is similarly unable to expand capacity fast enough.

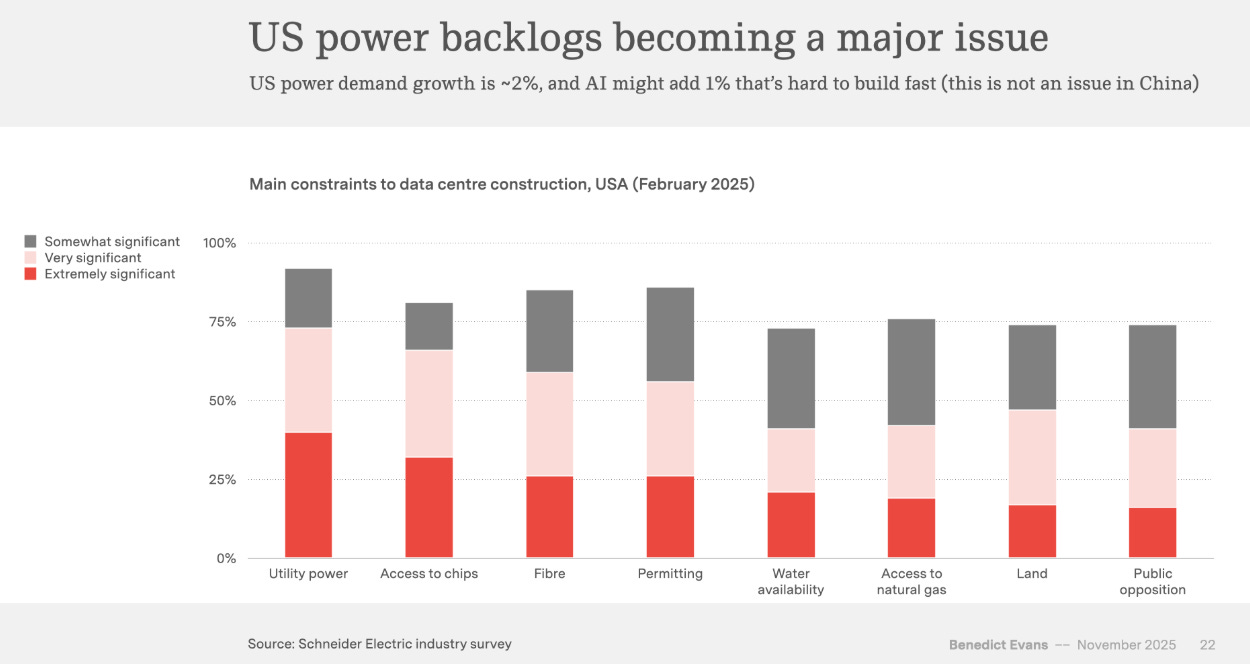

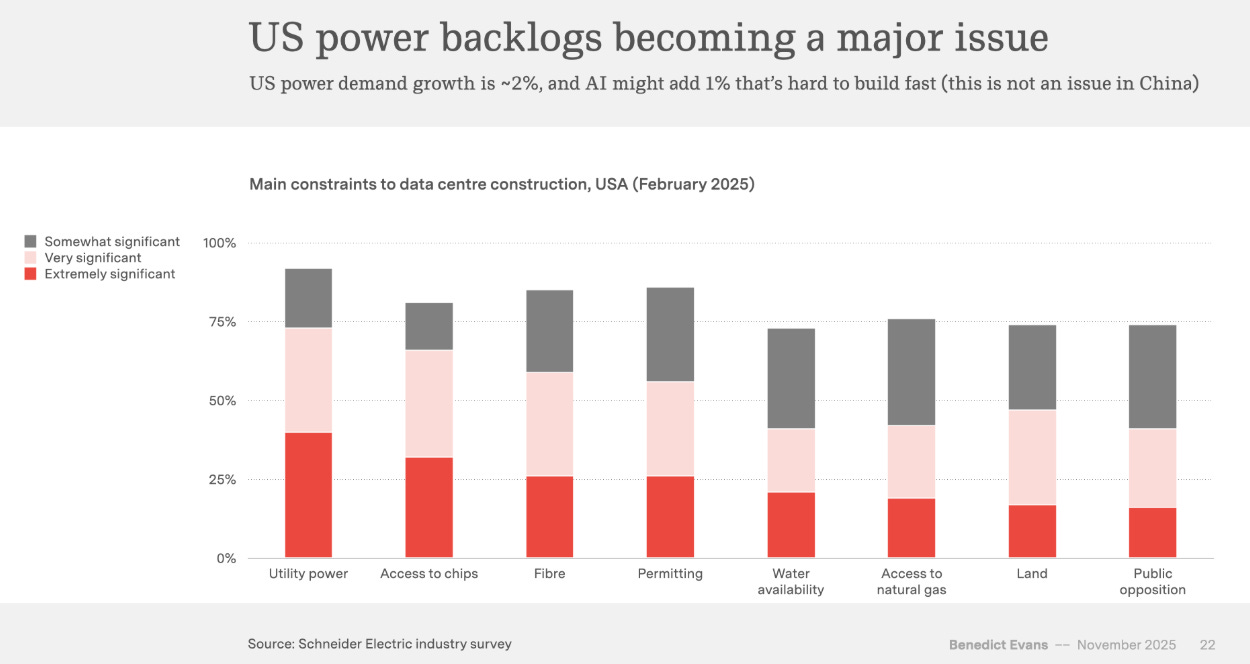

Evans, Benedict. (2025). AI Eats the World [Slide deck]. Power: For data center developers, particularly in the United States, “getting access to electricity is actually a bigger problem than getting chips from Nvidia.” Power backlogs have become a primary constraint on new construction.

Evans, Benedict. (2025). AI Eats the World [Slide deck]. This is not an issue in China, as it has surpassed the U.S. in energy production for years.2

Source: IEA, VanEck. Since 2005, China’s power output has increased nearly fivefold, with an average annual growth rate of about 8 percent. Meanwhile, the U.S., with a more mature infrastructure, has grown by less than 1 percent each year. In 2005, the U.S. generated about twice as much electricity as China; today, China surpasses the U.S., producing more than twice as much power.

Source: Bloomberg, VanEck. Power Generation, China and the U.S. (2005–2024). Especially in the industrial sector. Per VanEck: in 2023, industry absorbed nearly 60 percent of China’s final energy consumption, while in the U.S., commercial and residential accounted for more than 70 percent.

Source: IEA, VanEck. Construction: The physical challenge of building is immense. As Microsoft’s CTO, Kevin Scott, stated, it has been “almost impossible to build capacity fast enough since ChatGPT launched.”

Evans, Benedict. (2025). AI Eats the World [Slide deck].

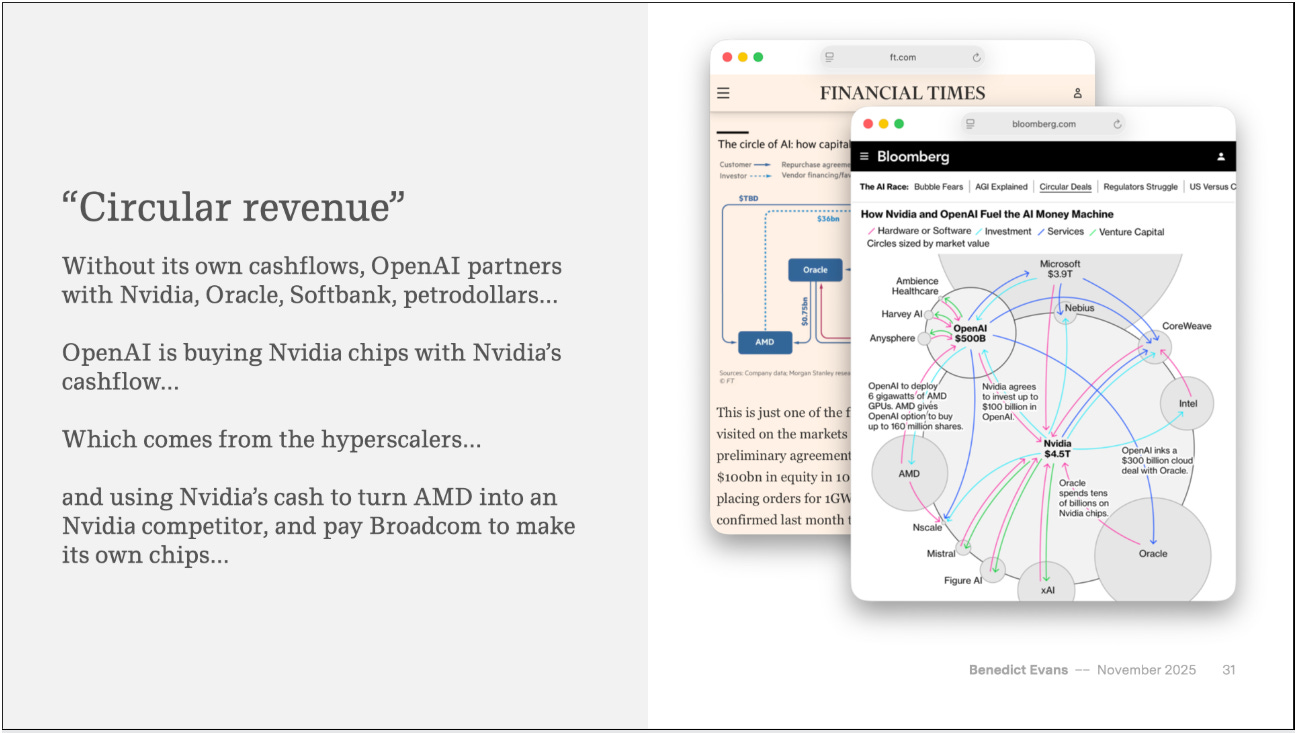

The Shift in Funding and “Circular Revenue”

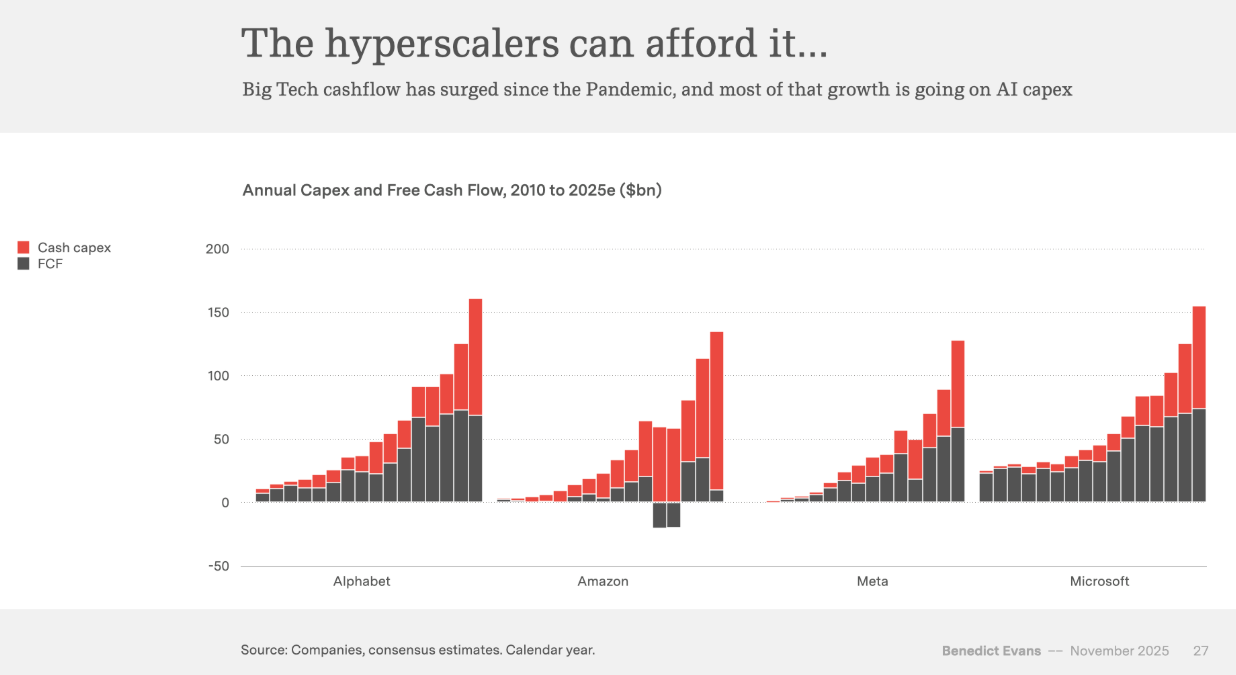

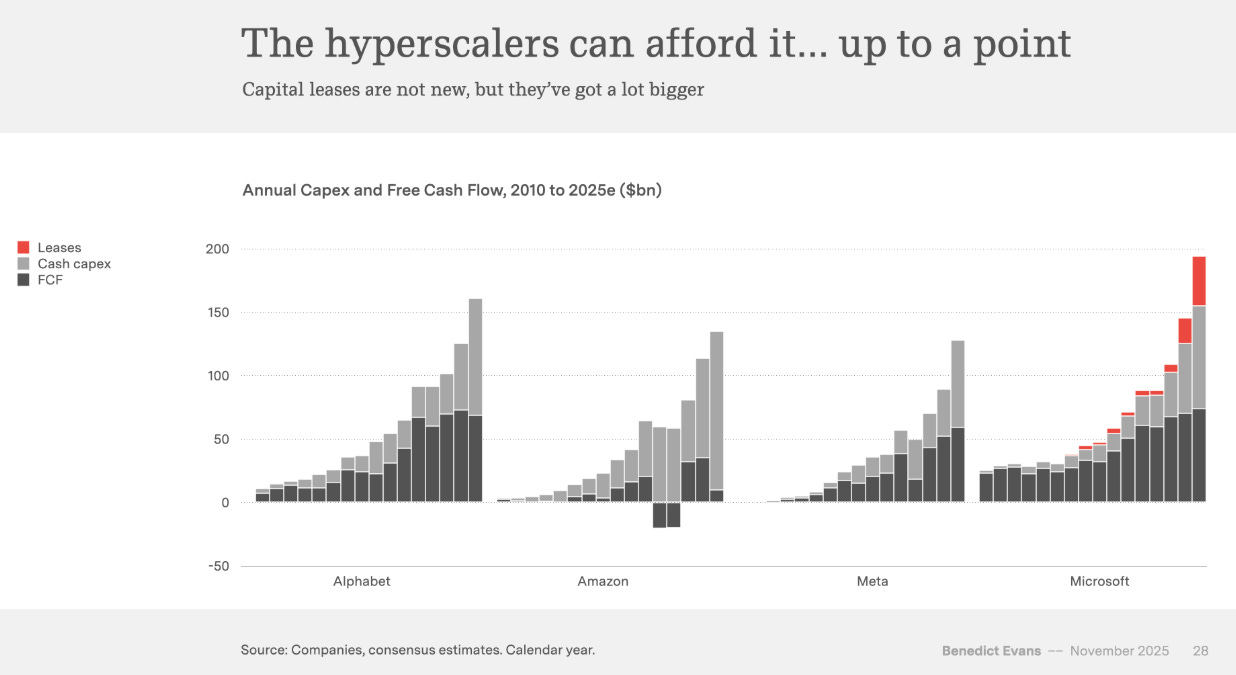

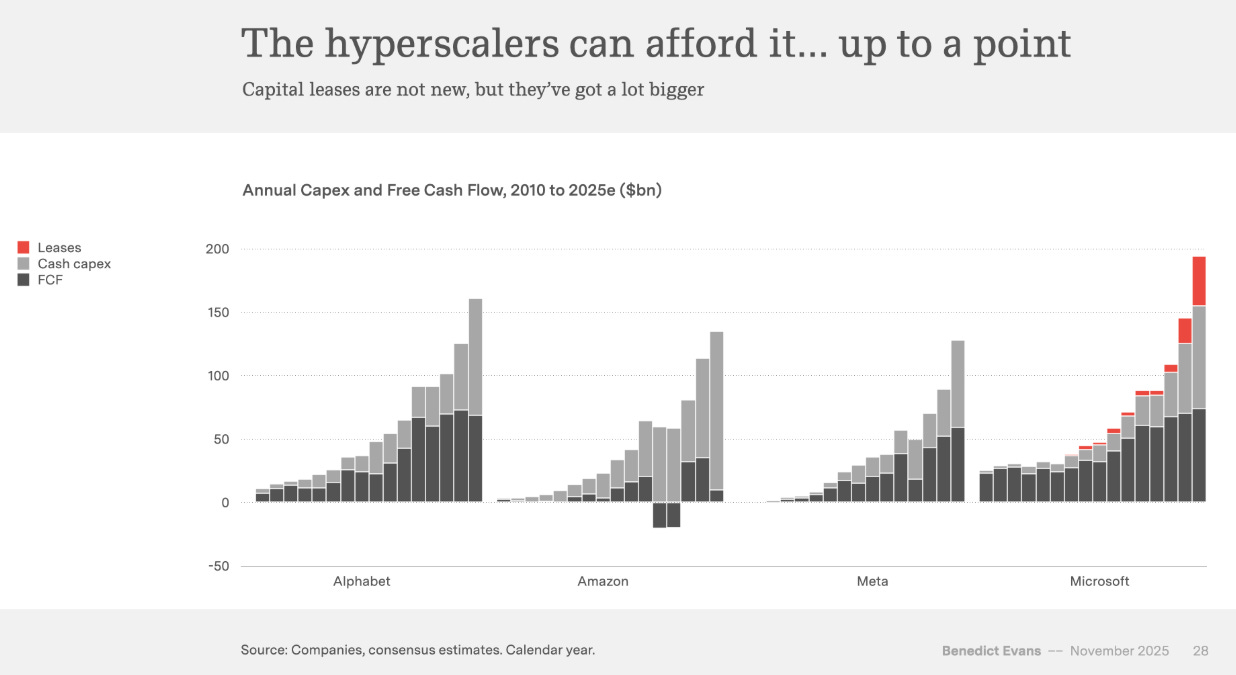

Initially, this capex boom was funded by the massive cash flows of highly profitable technology giants. However, the sheer scale of investment is now forcing a shift toward external financing.

Microsoft is reportedly engaging in approximately $50 billion of leasing in a single year to supplement its cash flow.

Evans, Benedict. (2025). AI Eats the World [Slide deck]. Meta has been cited in two separate data center expansion leasing deals, each valued at around $30 billion.

Oracle has seen suggestions that its cloud capex commitments might exceed 100% of its revenue, indicating a massive leveraging of its balance sheet.

OpenAI also joined the club, announcing commitments for 30GW+ of capacity at $1.4T3, aiming for 1GW/week of new construction at $20bn/GW or $1T annually4, which is equivalent to 2/3 of the total current global base every year. Part of it is the 10GW+ multi-year partnerships to deploy tens of gigawatts of capacity, including a 10 GW partnership with NVIDIA, a 6 GW agreement with AMD, and a 4.5 GW deal with Oracle as part of the “Stargate” project.

This dynamic creates a dizzying “circular revenue” loop: Nvidia’s own cash, derived from hyperscalers, is loaned to OpenAI. OpenAI then uses that money to buy chips from Nvidia to compete with the very hyperscalers who funded the transaction, while simultaneously funding Nvidia’s direct competitors, such as AMD and Broadcom. It’s a high-stakes, financially engineered ecosystem built on speculation and mutual dependence. This unprecedented capital burn forces the critical question: What, if any, defensible moats have been built with this mountain of cash?

Next lesson in The Economics of AI course

Lesson 3: The Competitive Landscape of Generative AI

Lesson 3 breaks down the commoditization of AI models, the lack of competitive advantages between AI companies, low user engagement, and the strategies companies are using to develop long-term, durable advantages and moats.

Let us know what you think

How do you use AI for work or personal reasons? Is it successful? What about your company?

Did we miss any other ways we should be thinking about AI?

What other businesses and industries do you think will be disrupted? How and why?

Share our community with others

We are building a community of innovators and proactive problem-solvers. Our aim is to establish a business and innovation incubator that supports individuals eager to innovate—helping them get started, connect with like-minded people, form teams, secure funding, and transform their ideas into tangible solutions.

Disclaimer

We reserve the right to change our minds about anything published in The Golden Age newsletter as new information comes to light.

Nothing produced under The Golden Age brand should be construed as investment advice. The contents of this publication are for educational and entertainment purposes only, and do not purport to be, and are not intended to be, financial, legal, accounting, tax, or investment advice. Investments or strategies that are discussed may not be suitable for you, do not take into account your particular investment objectives, financial situation, or needs, and are not intended to provide investment advice or recommendations appropriate for you. Before making any investment or trade, consider whether it is suitable for you and consider seeking advice from your own financial or investment adviser. This publication’s authors are not licensed investment professionals. Views expressed on The Golden Age are exclusively those of editors and not of any affiliated firm or organization. Do your own research before investing.

https://static1.squarespace.com/static/50363cf324ac8e905e7df861/t/69267317ffc0332dfc580e20/1764127511109/2025+Autumn+AI.pdf

https://www.vaneck.com/us/en/blogs/natural-resources/the-power-divide-china-us-and-the-future-of-the-grid/

https://www.reuters.com/sustainability/land-use-biodiversity/altman-touts-trillion-dollar-ai-vision-openai-restructures-chase-scale-2025-10-29/

https://www.axios.com/2025/10/28/openai-1-trillion-altman

Great read! The comparison between U.S. and Chinese energy infrastructure also brings to light a critical physical bottleneck: while chips can be shipped, gigawatts of power require long-term grid development that currently can't match the speed of software innovation.

As massive AI capex shifts from being funded by cash flow to external leasing and debt, at what point does the "circular revenue" model transition from a growth